Overview

For the last few months, as the world returns to normalcy from the COVID-19 Pandemic, along with the recovery of the economy in China and other parts of the world that have far exceeded initial projection, coupled with severe supply constraints, charter rates in the shipping industry have gone vertical.

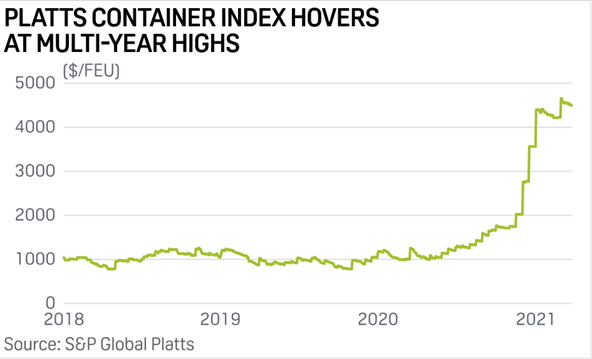

The effect is most clearly seen in the Container rates, which have since quadrupled, and, resulting in the share prices of some container shipping stocks increasing by as much as 12 times.

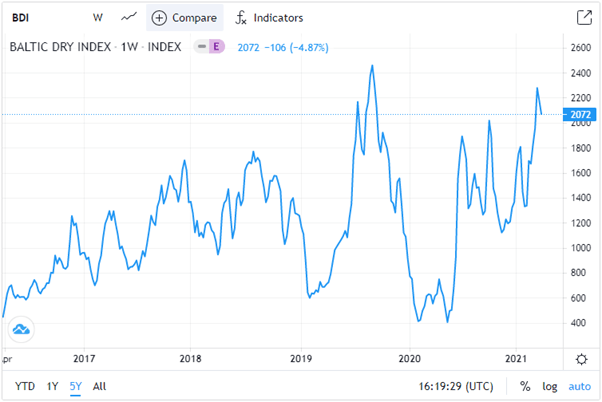

This strong increase in charter rates also applied to the bulk shipping industry.

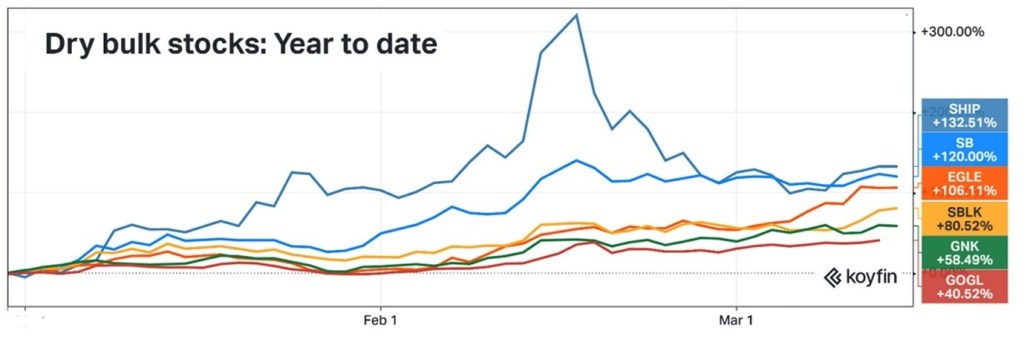

And like the stocks of container shipping companies, the stocks of Dry Bulk Carrier companies have also advanced strongly globally, with the share prices of a few companies rising more than 100%.

However, unlike the container industry which is a lot more homogenous (ie big container and small container ships carry the same type of containers/goods), the dry bulk carrier industry (and thus the Baltic Dry Index), consist of a few different classes of dry bulk carriers, who ship very different goods depending on the class of dry bulk carrier, and therefore have their own supply/demand dynamics.

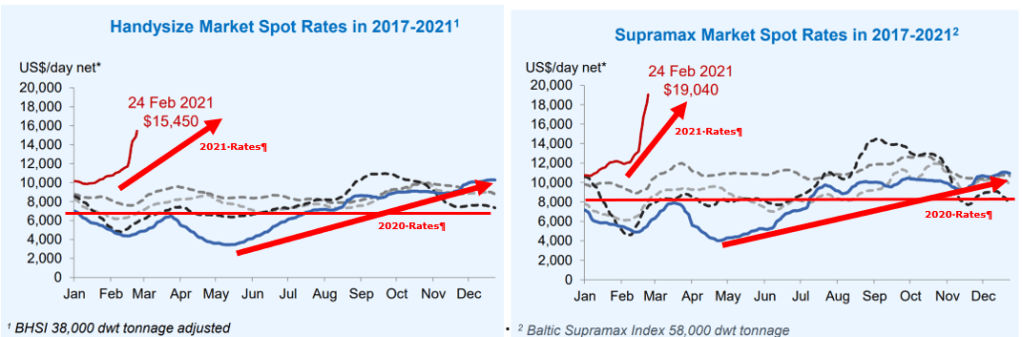

The charter rates of certain classes have risen far higher (Handy & Panamax ie Maybulk’s fleet) (and for some far slower, like Capesize) than what the index would indicate.

The Capesize ships for example, their increase in rates is not as obvious and have fallen significantly in 2021.

However, for the Handysize and Panamax sized ships (which Maybulk’s fleet consist of), charter rates have continuously increased in 2021, even before the Suez Canal Blockage.

*Handysize, Supramax and Panamax are the fleet classes whose rates have went and stayed up, due to demand for minor bulks.

However, despite only holding Panamax & Handymax ships whose rates have increased the most, the share price of Maybulk have barely moved, especially when compared against it peers.

And so, with the above in mind, we look at it from 3 different perspectives,

- Understanding the Dry Bulk Shipping Industry & Maybulk

- Sustainability of Current Charter Rates

- Impact of Charter Rates on Maybulks 2021-2023 Earnings

- Estimates and Global Comparative in Valuation

Understanding the Shipping Industry & Maybulk

For many people who have not studied the shipping industry, the shipping industry has been a “Holland” industry where every shipping company only make continuous losses, and there is a perpetual decrease in the share price. Unless your name is MISC and you have a permanent contract with Petronas.

The situation is so bad that today, there is zero analyst in Malaysia looking at the shipping industry.

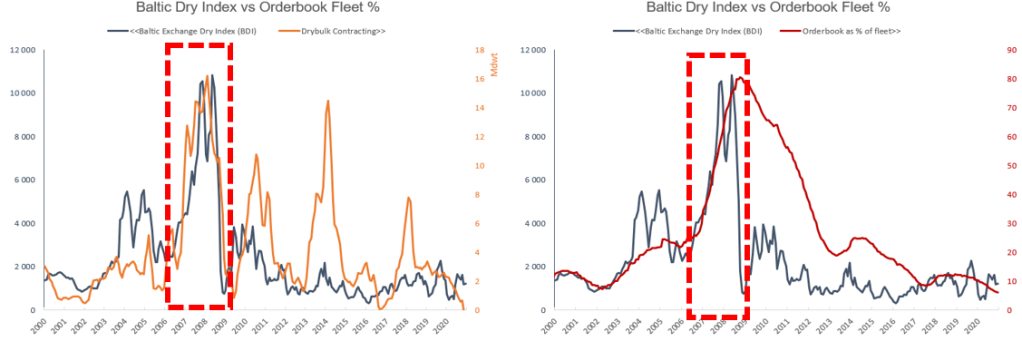

However, if one has studied its history, one would remember the 2000 to 2010 period, the golden age for shipping (as China started to rise, and therefore increased demand for commodities and its transport massively), and the subsequent overorders and oversupply resulted in the 2011 to 2020 winter for the shipping industry (which has instilled a certain kind of discipline and restraint in terms of capacity expansions).

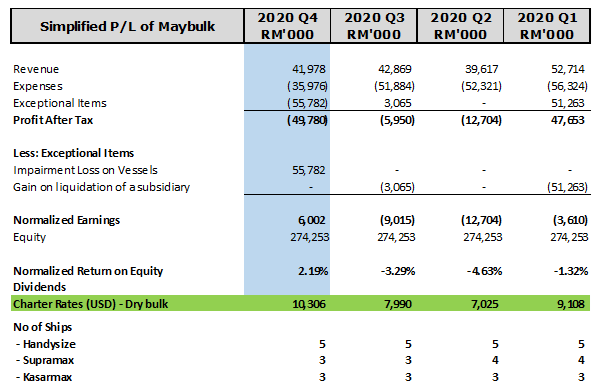

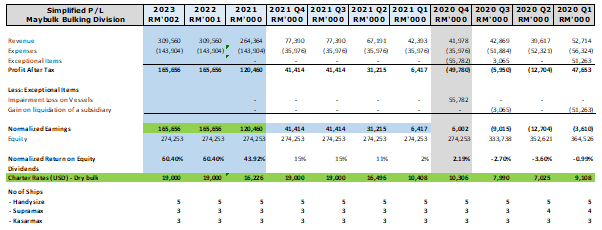

Looking at simplified historical earnings of Maybulk, we see the following.

The earnings during the golden age from 2003 – 2010 were incredible and so was the dividend payouts, which rose from RM19.5 million in 2003 to RM380.5 million in 2008.

The thing I found quite admirable about Maybulk (A Robert Kouk managed company), is how it was as early as 2005 that they expected an oversupply situation to occur, and therefore started to moderate their fleets, and so sold off old ships at very lucrative prices starting from 2005.

This proved to be a very wise decision, and most of the cash from the disposal of the ships was paid out as dividends.

The rest was used to diversify the company, via a RM792 million purchase of a 21.2% stake in PACC Offshore Services Holdings Ltd (“POSH”), (a provider of offshore vessels) at a valuation of around 10 times earnings. POSH did well initially and contributed RM64m in its first year as an associate. In 2013 & 2014, when bulking charter rates were all time low, POSH’s earnings contribution was the only reason Maybulk recorded a profit.

And so, in 2014, the company purchased an additional RM218 million worth of stock during the IPO of POSH in SGX to maintain its equity shareholding, bringing their total investment in POSH to RM1.01 billion.

Unfortunately, the fortunes of POSH is linked to the oil markets, which nosedived in 2015 and cont to make massive losses until it was privatized by The Kouk Group in 2019. Maybulk received RM251 million for its 21.2% stake, making POSH a RM759 million misstep.

And while the oil market was in a nosedive and POSH made large losses in 2015 – 2017, Maybulk was also looking at some of the lowest charter rates in the dry bulking markets history, as it was within its 10-year winter.

Which resulted in today, where there is no longer a single analyst looking at the shipping industry in Malaysia.

Since 2017, the charter rates of dry bulk carriers have occasionally recovered, but they have often proven to be a temporary.

Is the increase in dry bulk carrier charter rates this time sustainable?

Industries move in cycles, and after a 10 year winter, is it finally time for a spring upcycle in the dry bulk carrier market?

I think so, and here is why.

Sustainability of Current Charter Rates

Reason 1 – IMO 2020

On 1 January 2020, IMO 2020 came into play. This is a new regulation by the International Maritime Organization where a new global cap is placed on the sulphur content in marine fuels.

IMO 2020 mandates a maximum sulphur content of 0.5% in marine fuels globally (versus the current 3.5% sulphur content). The driver of this change is the need to reduce the air pollution created in the shipping industry by reducing the sulphur content of the fuels that ships use.

There is no way around this cap on sulfur emissions, as ports would turn ships away if they did not meet the required sulfur emissions cap.

Shipowners are given two options,

- Purchase Marine Fuel with 0.5% Sulfur content instead of 3.5%.

Except, Marine fuel with 0.5% Sulfur content is on average 70% more expensive than Marine Fuel with 3.5% Sulfur content.

Instead of purchasing 0.5% Sulfur Content fuel, IMO allowed ships to meet the 0.5% Sulfur requirement by having the ships install installed with exhaust gas cleaning systems or scrubbers.

Except, these are very expensive, and take up some space, reducing the amount of cargo that can be held.

In the face of persistently low rates for the last 10 years, as well as this new regulation which will increase voyage cost (or require higher capital expenditures), and the COVID 19 pandemic which reduced rates to below costs for already struggling shipping companies.

Many of them went bankrupt, and/or decided to sell the ships for scraps.

Even with order books at all-time lows, demolitions/scrapping for dry bulkers increased 80% year on year in 2020, taking out excess supply from the market.

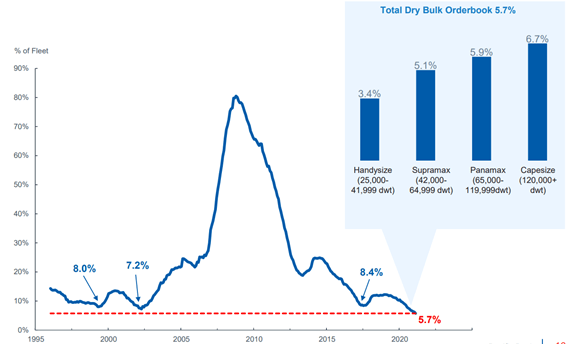

Reason 2 – Record Low Order Books

In 2021, order books for dry bulk carriers are at an all-time low, at just 5.7% of total supply. The last time order books were this low was in 2003, and it resulted in charter rates for Maybulk maintaining at USD 20,000 per day and flying to as high as USD 37,000 per day.

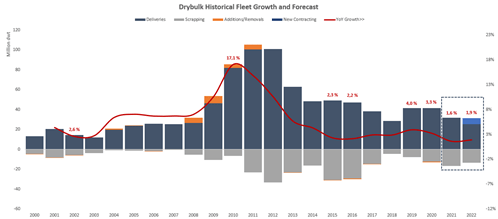

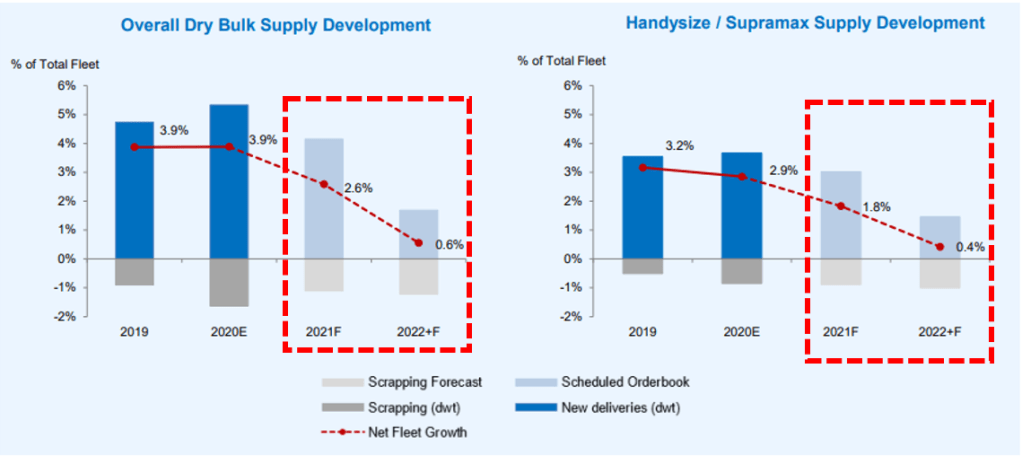

In 2021, net additions of new ships are expected to be all time low at just 1.6% of current supply, resulting in real supply constraints.

And based on current orderbooks of shipyards globally, net fleet growth is actually expected to further reduce in 2021 and 2022.

Reason 3 – Lack of Capacity at Shipyards & Time Needed to Build a Ship

Well, if there are not enough ships, why not just order it?

Except the 10-year winter in the shipping industry meant that many shipyards have either gone bankrupt or consolidated, resulting in significantly lower capacity.

And the strong increase in container rates, resulted in a strong increase in containership orders in all these shipyards, resulting in packed order books.

And even if you could place an order, the new ships will need 2-3 years to be constructed, which gives the dry bulk carrier industry a potential 2–3 year period of supernormal profits.

Reason 4 – China and US Infrastructure Stimulus

One of the key reasons for the current rally in charter rates, other than China’s faster than expected recovery, all time low ship order books, and record demolition of ships in 2020, is the USD 2.51 trillion infrastructure spending plan by China in 2020 to stimulate the economy.

This infrastructure spending have resulted in very high demands for commodities (which are transported by Dry Bulk Carriers), and the most obvious is in the record high iron ore prices.

High commodity prices mean suppliers are more than willing to pay high shipping rates to get the goods to customers as quickly as possible.

In addition, on 31March 2021, President Biden of the USA, announced a USD 2 trillion plan for infrastructure spending to improve the country’s infrastructure and boost the economy.

This is likely to further increase the demand in an already very tight market. Especially in terms of demand for grains in China following the recovery of its swine population after African Swine Flu in 2018-19, and high demand for construction materials and coal as government around the world begins to pump prime after covid induced recession, along with reduction in effective shipping and port capacity due to covid related restriction on seafarers.

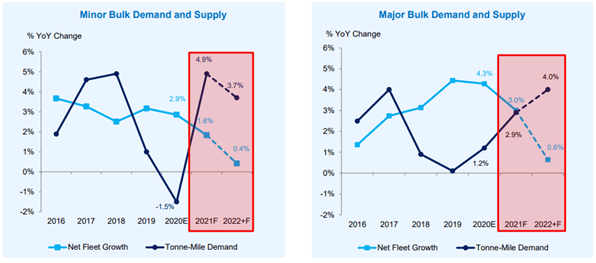

*Grains and Minor Bulks are the items usually transported by Maybulk ships.

If we were to look at current projections based on current/future supply (new ship buildings) and demand (recovery in economy and stimulus in China and US),

In 2021 and 2022, additional tonne-mile demand is expected to far exceed net fleet growth.

Impact of Charter Rates on Maybulks 2021-2023 Earnings

As we can see, Normalized Earnings and Charter Rates are very clearly correlated, and so, the question is, how does this affect the future earnings and how reasonable are my estimate?

And so, how much will the higher charter rates impact earnings moving forward? There are a few things to note,

- Costs are largely fixed, and therefore barring and increase in fuel costs that cannot be passed on to customers, every ringgit increase in charter rates is a pure profit.

- Over the years, the fleet composition of Maybulk have changed significantly. Even as recent as Q3 2020, an older jointly owned dry bulk carrier was disposed. And therefore, historical numbers do not mean much, except to give an idea of the management and the numbers.

- Maybulk’s ships are on short term charter which are 1-3 months long, therefore there is a 1–3-month lag before these rate increases is illustrated in the profit and loss.

- As new order of ships requires at least 2-3 years before they appear on the market, these assumptions are for 2021 to 2023.

- Based on our estimate, every USD1,000 increase in Charter Rates will improve Maybulk’s bottom line by around RM15m.

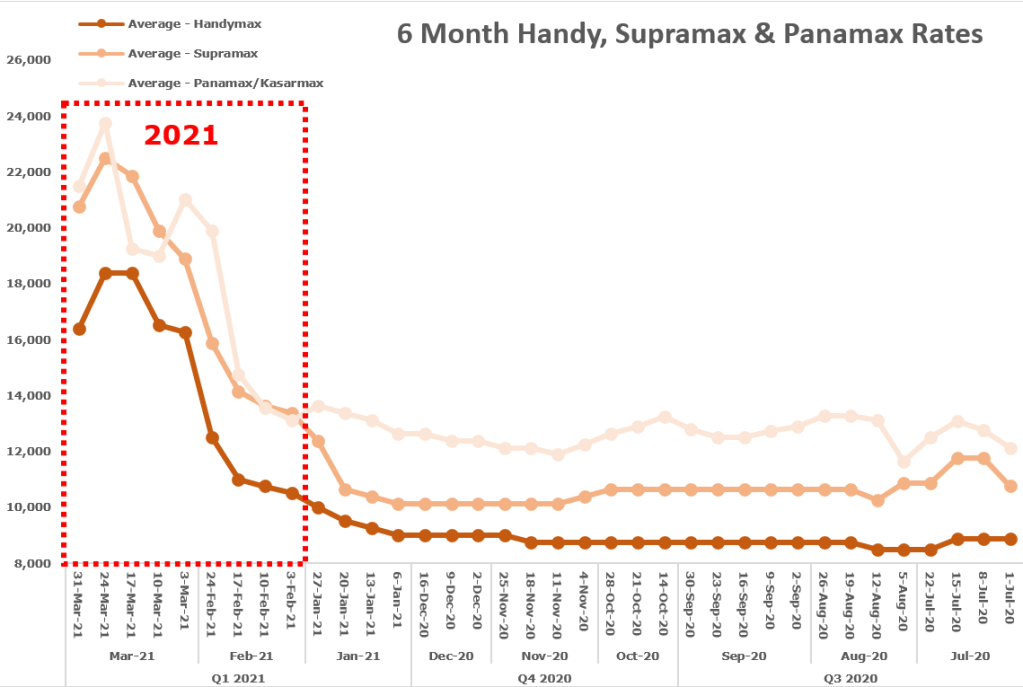

Above is the average weekly 6-month charter rates for Handy, Supermax & Panamax/Kasarmax rates.

They are usually split between Atlantic and Pacific Routes. To simplify things, we assume that Maybulk’s ships travel these routes on a 50/50 basis. Which gives the above benchmark average rate.

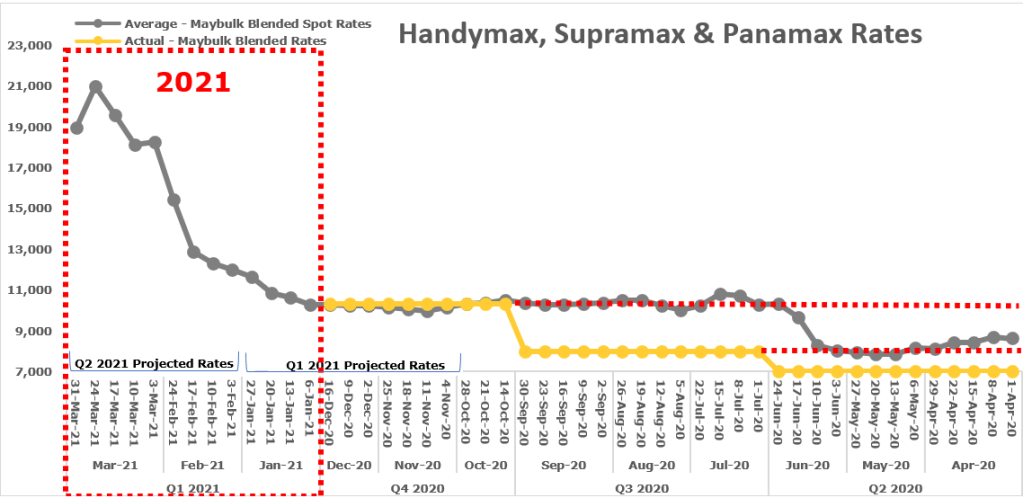

Next, given the rates above, we need to obtain the average rates which should have been obtained by Maybulk given their fleet composition.

When comparing the Average Rates weighted to account for Maybulk’s fleet composition, against the actual rates obtained by Maybulk each quarter, we note a 1–3-month delay. Why is that?

This is because like most dry bulking companies, Maybulks ships are typically on a 1–3-month charter, resulting in a 1–3-month lag in terms of the average rates obtained by the company.

And so, the projected 2021 Average Daily Charter Rates as follows.

Q1 2021: Projected using average rates from November 2020 to January 2021.

Q2 2021: Projected using average rates from February 2021 to March 2021.

Q3 2021: Rates are projected to maintain at elevated levels (but below the peak) from the cont strong demand from China as their economy recovery, as well as the rest of the world.

Q4 2021: Rates are expected to improve compared to Q3 2021, due to increased demand from the rest of the world as economies recover post covid, as well as the US’s USD2 trillion Infrastructure drive. However, to be conservative, I will be projecting the same amount as Q3 2021.

For 2022 and 2023, I will ignore the future catalyst to be conservative, and assume that rates maintain at USD19,000 (do note during the shipping boom in 2008, when order books were all time low, rates rose as high as USD41,000)

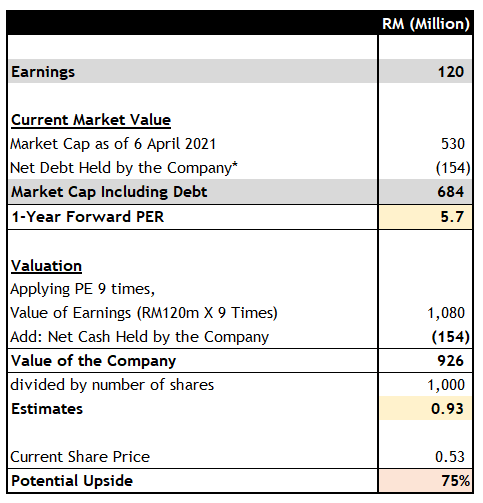

And given the conservative assumptions above, it appears Maybulk is likely to generate earnings of RM120 million or more for 2021. This amount should increase to RM166 million or so in 2022 and 2023 when the new ship orders is expected to come in. Post 2023, it will depend on the number of orders made in 2021 etc.

And given Maybulk past reputation of paying out large dividends in good times (Good capital allocation is standard when it comes to companies managed by The Kouk Group), this should also be the case in 2021 – 2023.

Lastly, the above also does not account for potential gain on disposal of ships, as the management have shown the ability to not allow euphoria to get to their heads and sell ships when prices are high (as done in 2007 and 2008).

Maybulks 2021-2023 Earnings Bonus (Upwards Revaluation)

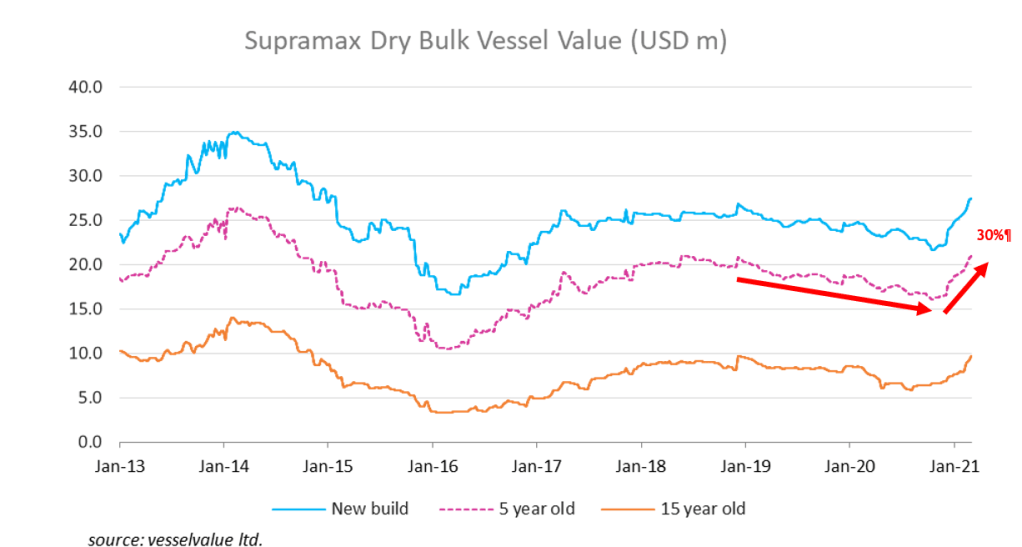

On Q4 2020, Maybulk was forced to record an impairment loss of RM56m on their ships last year due to Charter Rates due to the COVID pandemic, which resulted in lower vessel value in the market.

Since then, the prices of vessels around 5-year-old have increased by 30%.

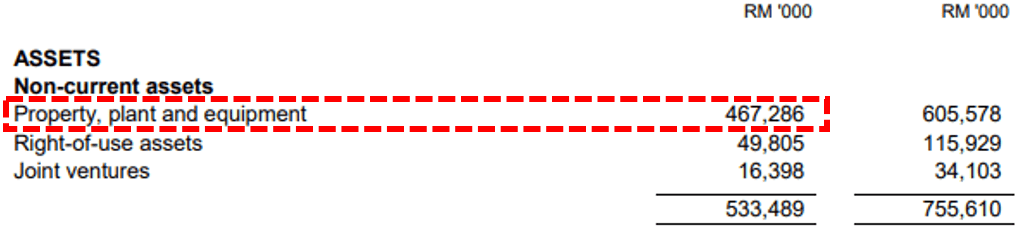

This means, the value of its ships, have increased by around RM 140 million in Q1 2021 (98% of its Property Plant and Equipment value is in vessels) in the current second hand market.

In terms of earnings, this may also result in a RM140 million write back in Q1. However, this is obviously just accounting numbers until it is disposed.

Estimates and Global Comparative

* Lease Liabilities are not included as these are basically rental expense that Maybulk pay every month for long term charters, and these amounts are already included as costs in the PL.

Given the above assumptions, we arrive at an estimate of RM0.93. These estimates appear reasonable as, rates are likely to be sustainable due to,

- All time low orderbooks.

- New ship orders only arriving 2-3 years from today.

- Insufficient current supply after large amount of bulk ship demolitions due to IMO 2020 and low rates in 2020.

- Recovery of the global economy

- USD 2.5 Trillion infrastructure stimulus in China resulting in large demand for commodities.

- USD 2 Trillion Infrastructure Stimulus from the US not being priced in rates wise to provide a margin of safety.

- Maybulk’s Ships are very new, and have scrubbers installed.

- Significantly higher demand for construction materials and coal as governments around the world begins to jumpstart the economy via infrastructure stimulus (the most common way) after a covid induced recession.

And lastly, I believe my estimate have a large margin of safety, as earnings in 2022 and 2023 likely to be more than RM160 million, which is much higher than its projected 2021 earnings of RM120 million, but this is not included in my estimates.

Well, the second question is how does Maybulk compare globally valuation wise?

On a EV (Enterprise Value: Market Capitalization Plus Debt Less Cash) per DWT’000 basis, when compared against its peers, Maybulk is trading at a 37.3% discount compared to the average of its peers.

When compared against its most similar competitor, Pacific Basin (In terms of fleets, Pacific Basin is almost purely Handysize, Supramax and Panamax like Maybulk, and the fleet is as young as Maybulks), Maybulk is trading at a 62.1% discount to Pacific Basin.

Key Risks – Selling By Bank Pembangunan

Back when Maybulk was first formed, Bank Pembangunan was one of its key shareholders. Recently, for one reason or another they have started to dispose their shares, which resulted in the share price of Maybulk barely moving compared to its peers globally.

In December 2020, before the disposals started, they had around 185 million shares. After continuously disposing during the initial run up, and daily in March and April, they currently hold just 100 million shares.

However, despite the steady selling, which often consist of half the traded volume every day, the share price has been on a steady (albeit a little slow and volatile) uptrend. Clearly many large buyers have been collecting.

To paraphrase a quote, “The Truth Always Prevails”. The slower than peer increase in share price is an opportunity for many of us to enter the company much cheaply, while in time, the supply shortage in the bulk carrier industry, the future super normal profits and high dividend payouts (as per the Kouk Group Standard) will eventually prevail.

In any event, with only 100 million shares left on 8 April (Should be only 90mil after the selling on 9 April), I expect Bank Pembangunan to finish selling within 10 – 15 workings days depending on trading volume. And like taking the cork off a bottle of champagne, the subsequent increase then is likely to be quite violent.

One Last Tong (Thing),

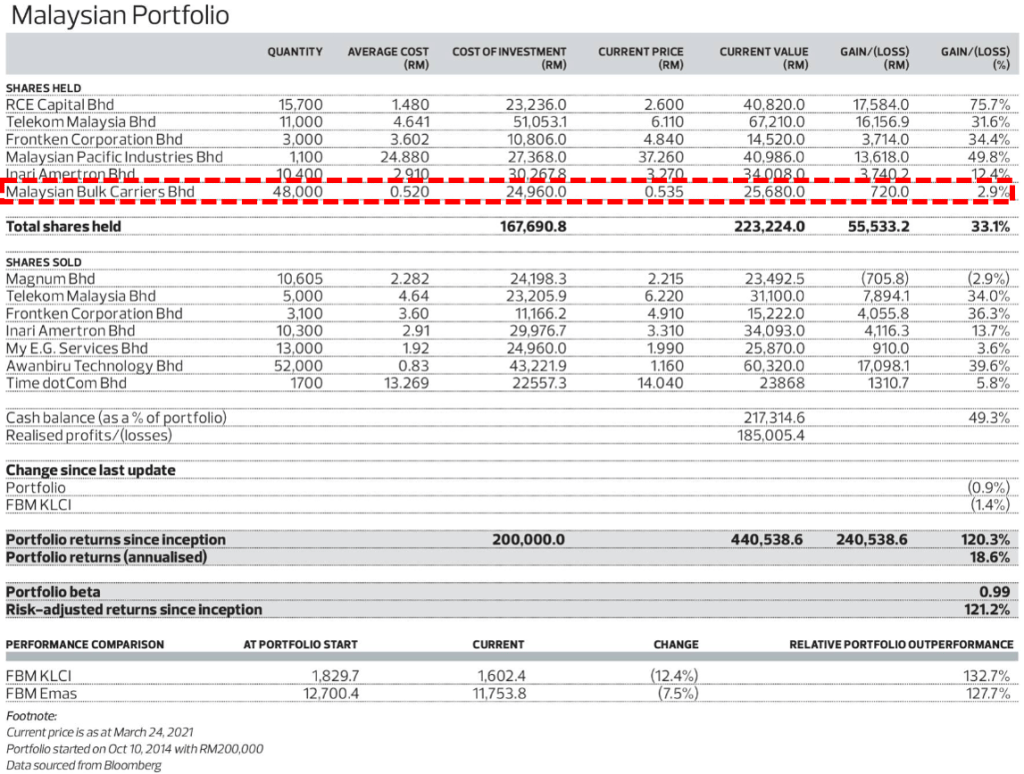

One of the portfolio’s I look at with great interest is the one by The Edge’s founder, Tong Kooi Ong, and as we can see,

Around 2 weeks ago, Mr Tong have purchased some shares. On a personal level, I find a certain level of additional comfort (on top of my own research) when people whose thought processes I admire are on the same boat.

Given all the above, I am quite comfortable with my thesis and estimates of the value of Maybulk.

Hi Choivo, may I ask why Maybulk has been dropping last few days? Qr should be announced next week if I’m not mistaken. Care to offer some pointers?

LikeLike

This post seems to aged well given 1H 2021 result out and thesis remain intact. Fleet disposal was as per your expectation and hopefully shareholders can benefit through dividend payout. Just want to note it was quite a dissapointment when Mr Tong didnt hold the stock for long and sold it for a small gain with no reason stated whatsoever.

LikeLike

Who is Mr Tong? Or do you mean Mr Tho the CFO? Shipping lines had suffered a long 10+ years of recession. Think the board are trying to do some costs cutting by selling loss making vessels in the year 2020 and 2021 to cater for more rainny days ahead. Shipping rates in 2021 has been going through the roof almost doubling to the forecast of the author in this column due to continuing ports congestion, increasing demand in coal, iron ores, metal, copper and other PPE materials. With the abrupt shutdown of Ningbo port in Shanghai this week, this will only create more port congestions in and out of china. Indirectly this may prolong the up cycle of the ship chartered rates. The author projected a 2021 profit of Rm 120 mil which is well under way. The bonus may come from the vessel disposal gain from the 3 August 2021 sales of Rm 280 mil. Maybe a handsome disposal extraordinary gain in the region of Rm 100 to 140mil may be added into 3rd quarter 2021 earnings. Since the board thinks the ships value have appreciated 75% from year 2020, we may see a revaluation in the region of Rm 200mil come 4th quarter instead of the impairment loss of Rm 50mil. Are the shareholders ready for a profit of between Rm 220 to Rm 450 mil for the full year 2021? If so, should the share price be at Rm 0.72 or Rm 2 to Rm 3???

LikeLike

I am referring to Tong Kooi Ong (The Edge’s founder) in Choivo’s last part of the article above, since Choivo mentioned it was reassuring that Tong also had it in his Value Portfolio.

The disposal gain is one off so I certainly dont think it will go up to RM2. And with the disposal, Maybulk is left with 5 vessels only so there will be reduced earnings in the future.

LikeLike

Fair enough. Any idea whether Bank Pembagunan has sold out all their holdings? Seems volume on this counter has been dropping ever since news reported they had cut their holdings to below 5% 3 months ago. Just wondering who had picked up their 18% stake? Whoever it is must have a strong bullish stand on the counter.

Any idea where their ships are parked when they are idle? I noticed many investors selling down on this stock whenever our govt announced new EMCO or tougher MCO measures. If their fleets are mostly sailing or chartered out, this should not affect anything at all right?

In their company report, they mentioned got 2 vessels are under Long Term chartered. Does this mean the sailing rates will be committed on leasing date and cannot be revised upward in the committed period? Any idea what rates they are?

LikeLike