Overview

When I first wrote about MBMR, it was RM 2.85. Since then, it has increased to a high of RM3.73, before settling down back at RM3.4 (far below my Target Price).

This is despite my prediction of record earnings coming true, due to Perodua’s Monthly Sales having broken their 27 year record for 2 consecutive months as this pandemic has changed the way people travel and their modes of transportation (with the virus around, people who previously used public transport, now much prefer using their own vehicles) which have resulted in increased demand for vehicles, along with the SST exemptions.

Part of this I believe is due to the Malaysian Public not fully understanding the Car Industry in Malaysia and the incredible edge given to car manufacturers like Perodua and Proton.

Understanding the Car Industry in Malaysia

In 1983, as part of Malaysia’s industrialization drive, Proton our first national car manufacturer was incorporated, and a series of import and local taxes was implemented to support Proton (and Perodua which was incorporated in 1993).

Over time, Malaysia slowly stopped having a national car policy, and companies like Proton and Perodua become privately owned with GLC links.

However, as the tax collected from cars now amounted to more than RM10bil a year and a significant source of revenue for the country, they continued to be implemented. They are as follows,

Definitions:

CBU: Complete Built Up – Imported Fully Finished

CKD: Complete Knocked Down – Imported in Parts and Assembled Locally

MFN: Most Favoured Nation Status

ATIGA: ASEAN Trade in Goods Agreement

And computed as follows,

Selling Price of Cars: Open Market Value (“OMV”) X Import Duty X Local Taxes

For CKD: OMV is defined as final market value of a CKD vehicle ex-factory.

For CBU: OMV is defined as Cost, Insurance and Freight (“CIF”) of the vehicle.

Taxes for CKD are lower vs CBU cars, as the Malaysian government would like to incentivize the development of car related industries in Malaysia and provide jobs locally, and these import duties are applied EQUALLY across the board for all car manufacturers in Malaysia.

However, Ministry of International Trade and Industry (MITI) also offers various grants to car companies, both foreign and local, to promote value added activities like research and development and vendor development, like

- The Industrial Adjustment Fund, and

- Automotive Development Fund

All car companies that carry out CKD local assembly of motor vehicles qualify for these grants. There is little specific detail on how these grant amounts are determined, however, they key criteria are,

- Value/Number of Cars sold

- Amount spent in terms of Research and Development in Malaysia

- % of Local Parts Content in the cars.

These grants are used to off-set the actual excise duty paid through Customs and are the main reason why Perusahaan Otomobil Kedua Sdn. Bhd. (“Perodua”) and Proton have a huge edge versus all foreign competitors.

Now, the local players have an edge over the foreign players in 2 main ways.

- If you were to study the car industry, the commonly accepted optimal efficient scale of economies is around a minimum of 400,000 units/year.

But as consumption in Malaysia is far lower and we have low vehicle exports, it is impossible for foreign manufacturers doing CKD cars in Malaysia to achieve economy of scale to make prices competitive with Perodua.

Perodua manufactures more than 200,000 cars a year, while foreign manufacturers like Honda, Toyota etc can only manufacture less than 100,000 cars a year for local consumption, and the amount is dropping each year as price differentials become more obvious.

Resulting in a vicious cycle where the prices of their cars become even more uncompetitive due to lower economy of scale.

- Proton and Perodua will always receive more grants (which lowers the tax payable) than the foreign players for a few reasons,

Firstly, As Malaysia is the home base for Proton and Perodua, there is every incentive for them to spend R&D in making sure local content is high, increasing production efficiencies, and customizing vehicles for local markets.

This is not the same for foreign manufacturers who are already spending billions in R&D in foreign countries, for them to spend it here would be to do double spending for what is a small market for them. Currently, Perodua is the biggest spender in R&D in Malaysia for motor vehicles, which is why the grant they get is also the biggest.

Perodua basically spends all their time building up the local car manufacturing/parts industry in order to get high local content to obtain much higher grants.

This is something that the foreign companies do not do as much, as their main manufacturing base for ASEAN etc is in Thailand, and again Malaysia is a small market.

Currently the car with the highest local content in Malaysia is the Perodua Ativa SUV (95% local content) and previously, it was the Perodua Myvi (90% local content).

- And lastly, for CKD cars, An assortment of components determines the OMV, and these include the cost of the CKD pack, cost of manufacturing and components as well as assembly and administration charges.

Based on new regulations issued on 31 December 2019 in a MOF gazzette by the Government to determine OMV, the computed value to determine duties will now take into account not just the profit and general expenses incurred or accounted in the manufacture of a vehicle, but also of its sale.

As specified in clause 4.2 (d) “any direct and indirect costs incurred or accounted in the manufacture and sale of the dutiable goods.”.

This would result in CKD cars (especially those by foreign manufacturers) costing 10-15% more, widening the value and price gap between Perodua and the foreign manufacturers.

And what this basically resulted in, is this industry being dominated by two players. Proton and Perodua, who have the cost and value advantage.

(As for Proton, before Geely acquiring the 49% stake, instead of selling rebadged cars, they spent money trying to make their own, which resulted in a far inferior product offering, resulting in all their advantages being thrown away.

It is impossible to design and manufacture a car from scratch profitably if your only market is Malaysia)

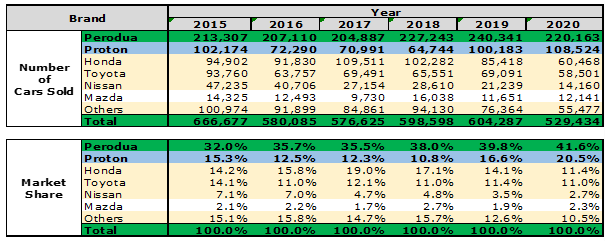

Despite declining number in vehicles sold in Malaysia from 2015 (666,677 cars) to 2019 (604,287 cars.).

The number of vehicles sold by Perodua have increased from 213,307 cars in 2015 to 240,341 cars in 2019. Increasing market share from 32% in 2015 to 39.8% in 2019. Peroduas market share in 2020 have further increased to 41.6%.

Proton (Geely) versus Perodua (Toyota)

Now, one of the main concerns the market has about Perodua today, is how competitive it will be compared to Proton, after its rejuvenation by Geely.

Proton have basically changed its business model completely and started copying Perodua by selling rebadged cars by using Geely’s portfolio.

However, the key thing to note here is this.

Proton’s real competitor is not Perodua, it is the foreign manufacturers.

Since Proton’s rise in 2019 and 2020, Perodua have actually gained market share. The real and biggest victim of Proton is Honda (their HRV can basically throw rubbish bin), and all the other foreign manufacturers who have lost market share, and vehicle volume.

If you look at the price points of Proton/Geely’s new models,

Proton X70: RM95k – RM123k

Proton X50: RM79k – RM103k

against Perodua’s new models

Perodua Aruz: RM68k – RM73k

Perodua Ativa: RM62k – RM72k

The new Proton models are targeting the aspirational part of the market who would otherwise buy a car from a foreign brand, while the Perodua models are clearly targeting their bread and butter, which is the M40 & B40, the largest segment in the market, which also places a high level of importance on fuel efficiency.

Again here, the Ativa is far more fuel efficient at 5.3L/100km versus 6.5L/100km of the X50. This is also consistent when comparing their most popular vehicles.

The cheapest (all-in ownership cost) and most fuel-efficient car in Malaysia is the Perodua Bezza 1.0 G (A Proton Saga 1.3 Base is cheaper by about RM2k but is 30-40% less fuel efficient). Which is also why it is the best selling car in Malaysia.

Catalyst 1 – Perodua Ativa / Daihatsu Rocky / Toyota Raize likely to sell very well

On a very fundamental level, this is a competition between Toyota and Geely in Malaysia. Some people may say it is Daihatsu, but Daihatsu have been acquired by Toyota 2016, and many of the cars in Toyota & Daihatsu share the same platform or engine, and the Perodua Ativa is no exception. In Japan, the Perodua Ativa is also known as the Daihatsu Rocky and Toyota Raize.

Now, the biggest question on everyone’s mind is, how will it do compare to Proton X50?

Now, the Perodua Ativa was only launched less than 3 weeks ago, and so information is quite sparse, beyond anecdotal information I’m getting from Perodua car dealerships who tell me about customers who cancelled X50’s for the Ativa.

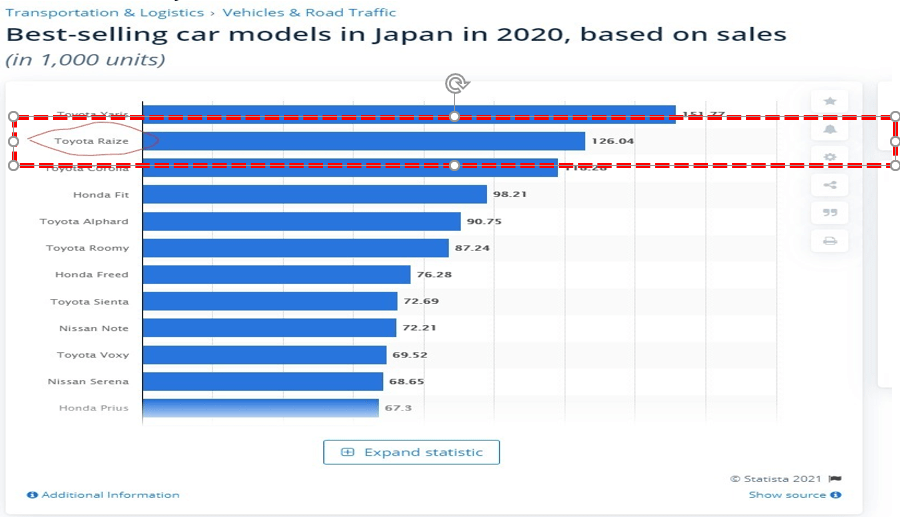

To really get some solid data, we need to look to Japan, where the Toyota Raize and Daihatsu Rocky was released in November 2019. How were the sales?

In 2020, the Toyota Raize is the second best selling car model in Japan (one of the most competitive car market in the world), when combined with the numbers of Daihatsu Rocky (it’s the same car), it’s the best selling car model in Japan for 2020.

This car is a complete runaway success in Japan.

How will it perform against the Proton x50/Geely Binyue/Geely Coolray?

Well, in short, good luck finding a Geely car in the top 20 of Japan best selling cars for any of the years.

But to take it more seriously. The Perodua Ativa offers Level 2 Autonomous driving capabilities from the Perodua Ativa AV model, which costs RM72k. To get this same feature in the X50, you need to purchase the Proton X50 TGDI Flagship, which costs RM103k. A difference of about RM31k, enough to buy a Perodua Bezza

In addition, the Perodua Ativa also sells for a lower price in Malaysia, than what the Daihatsu Rocky or Toyota Raize sells for in Japan (RM71K-RM86K) than in Malaysia (RM62k-72k) I think it will do very well.

Catalyst 2 – Higher Dividend Payouts

As we all know, the main value in MBMR lies in its 23% stake in Perodua.

And over the years, its earnings have remained consistent due to its, monopoly/duopoly like position from the structural costs and value edge it has over foreign manufacturers, and these earnings have only increased in 2018 and 2019 due to the increasing price and value differentials versus the foreign manufacturers.

Now, Perodua is owned by, UMW Corporation (38%), Daihatsu Motor Co. (20%), Daihatsu (Malaysia) (5%), MBM Resources Berhad (22.6%), PNB Equity Resource Corporation (10%) and Mitsui & Co. (4.4%). The fact that no one holds a controlling stake also means that 60-70% of Perodua’s earnings are usually paid out as dividends.

Unlike companies like DRB-HICOM, who has many other businesses, many of which are loss making during this COVID period, and thus mask the increased earnings from PROTON. The earnings and dividends contributed by Perodua is usually around 75% of MBMR’s earnings and cashflow.

However, despite recording explosive earnings in Q3 and Q4 in the midst of the pandemic, MBMR is currently selling at RM3.4, far below its Pre-covid valuations of RM4.0 and is selling at just 4.5 PE today.

Earnings Versus Dividend Payout

Historically, despite large dividends by Perodua to the MBMR, the dividends paid by MBMR is usually lower, why is this the case?

As we can see here, this is mainly due to a large loan taken out in 2011. Since then, the reduction in dividend pay-out was mainly due to cashflow being diverted to pay off this loan.

When the MBMR turned strongly net cash in 2019, dividends payment tripled to RM58.6m from RM17.6m in 2018. In 2020, despite lower dividends from Perodua due to timing difference, (Perodua dividends is paid out 2-3 times a year, and is calculated internally as 70% of earnings. As Q1 and Q2 2020 profits are low during the pandemic, the dividend is lower. However, as the profit subsequently increased substantially in Q3 and Q4, the dividend payout should again increase and will be seen in the 2021 Q1) dividends have further increased to RM82.1m.

In addition, as we can see here, the other segments of MBMR usually generate additional cashflow as well. So why was the loan taken out in 2011, and will this occur again and reduce future dividends?

Why was the loan taken out in 2011?

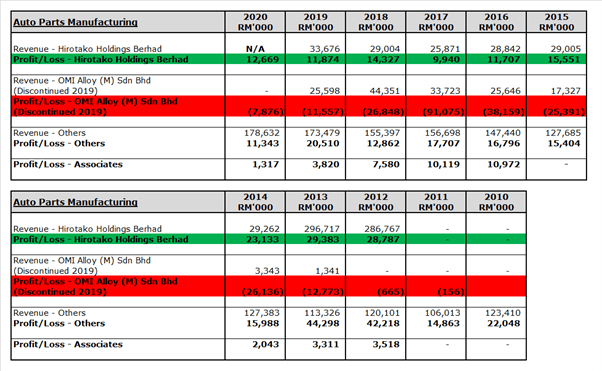

In 2011,a loan of RM370m was taken out by MBMR for the privatization of Hirotoku Holdings Berhad which cost a total of RM410 million (to this day, this company is run by the Japanese Partner). This company is primarily in the business of manufacturing Acoustic and Safety Products for vehicles.

In addition, in 2012 the company also started OMI Alloy (M) Sdn Bhd, an alloy wheel manufacturing company. Both companies are under the Auto Parts Manufacturing Segment. How has these companies performed over the years?

For Hirotako Berhad, earnings have fallen somewhat since the glory days of 2009-2013, however it is still quite profitable. However, the lower profitability did require a write off on goodwill in 2017.

But for their alloy wheel manufacturing company OMI Alloy (M) Sdn Bhd, it performed badly due to China flooding the market. This loss-making division have been shut down in 2019 and would no longer result in losses for the company.

What about their other division, the Motor Trading Division?

Its profitability fell during the 2013-2017 period but have since risen again to all time highs due to the release of the Perodua Bezza. The contribution by Perodua have also increased to record highs.

Both segments are likely to contribute positively to the record earnings to be recorded by Perodua in 2021.

Dividend Payout?

The question now is this.

Will most of these profits be paid out as dividends, or used to purchase other companies or PPE?

There are a few things to note.

- With the borrowings being fully paid off, it would be reasonable to think that a significant part of the additional cashflow will be used to pay dividends, as they have shown in tripling the dividend payout to RM58.6m from RM17.6m in 2018. And in 2020, it was increased another 40% to RM82.1m

- Back when they acquired Hirotoku Berhad, the car parts manufacturing business was a good one, this was before china came into the picture. Given the economics today, this industry is not very attractive anymore.

Which are also why PPE purchases by MBMR have been quite low over the years indicating that only maintenance capex is spend, with there being very little expansion plans. After the OMI Alloy fiasco, I think they are very content to run the current business and distribute dividends from Perodua.

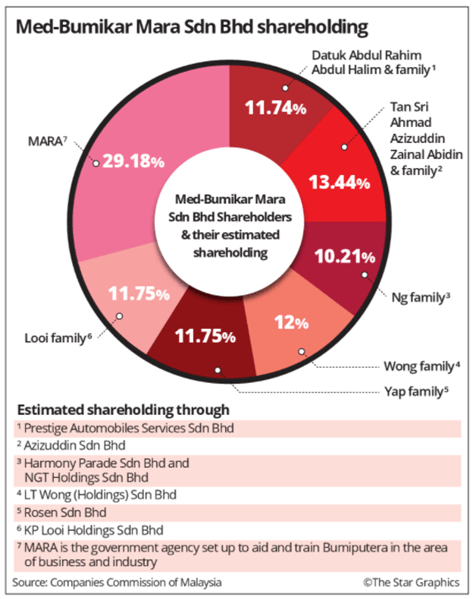

- The 50.2% owner of MBMR is Med-Bumikar Mara Sdn Bhd. Like Perodua, there is no controlling owner. 70% of the shares are controlled by 6 different families who have entrepreneurial/business background. Given that no one has control over the company, historically, any additional income would likely be distributed out, so the respective families can do whatever they want with it.

With these in mind, I think that for the FY2021, at minimum RM170m (60% of earnings as guided by management in 2019) would be distributed as dividends by MBMR, this translates to 10% dividend yield.

Estimates

To perform an estimate of the value of the company, I will annualize 2020 results using the two most recent quarters Q3 & Q4 2020, as I believe the good results can be sustained somewhat due to the Perodua Ativa launching successfully.

Given the large rerating (from a NBV basis, to one valued on a PE and dividend basis), a larger 30% discount in relation to margin of safety is applied.

Great writeup! One thing to note though is that the current explosive sales volume for Q3&Q4FY20 is due to the SST exemption which will end in June this year. Sales would definitely strongly taper off starting from Q3FY21 as those who want to purchase would have already done so, which would in turn affect the div payout of Perodua. Curious to know why was this not taken into consideration for your FY21 earning estimates?

LikeLike

I trust people will be able to do their own estimates.

I follow the thinking that you dont need to know the weight of the woman to know if she’s fat, or the height of a man to know if he’s tall.

A good investment should be very obvious, and i think this one is.

LikeLike

If you recall back in 2018, there was a period GST holiday after Pakatan Harapan took over and decided to abolish GST, the sales number for Perodua only dropped sharply for 2 months (AUG & SEPT 2018) and recovered to normal level.

LikeLike

Brilliant analysis. This has become my favourite site for bursa shares analysis

LikeLike

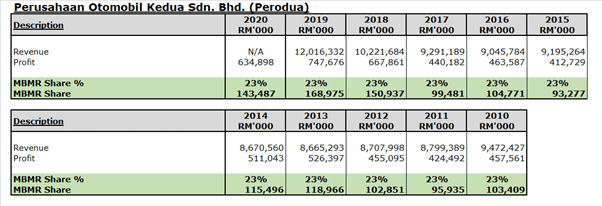

Hi Jonathan, thanks for the insights. I’m trying to do my due dilligence before adding more position onto this stock. May I know where did you find the Revenue and Profit figure for Preodua Sdn. Bhd.?

LikeLike