Overview

One of the bright spots in the market over the last few months have been in the Solar and Technology Companies.

However, one of my favorite utility companies who is,

- Sole water concessionaire in Johor (and one of the only profitable water utility in Malaysia) with ingeniously designed contracts and incentives;

- Power concessionaire supplying 37% of the power in Sabah;

- Strong water related technical capabilities with water related EPCC (Engineering, Procurement, Construction and Commissioning) contracts and water assets all over the world.

- China: 12 Wastewater treatment plants ranging from 25-30 years with total treatment design capacity of 227 MLD.

- Thailand: 10 Water, wastewater treatment plant and reclamation water treatment plant with total treatment design capacity of 114 MLD.

- Designed a Non-Revenue-Water (Basically Water Wastage) saving system called “AquaSmart”, which is utilized successfully all-around Malaysia. In Johor alone, usage of their system has resulted in NRW going from 40% to 24.1%. And this is despite 7,000 km of pipes in Johor being asbestos cement pipes that were installed 40 years ago.

Success cases like these make me think they have a good shot at the RM4bil Rasau treatment plant tender next year. - Participation in the LSS4 Tender called by Suruhanjaya Tenaga. In 2018 they participated in the LSS3 Tenders but was not successful. Given their experience and learnings from the LSS3 tenders, as well as their great track record thus far in the water and power industry so far, makes me think their chances for LSS4 is decent.

- Last but not least, 6% dividends, while maintaining pay-out ratios of just 50-60% giving further upside potential.

Malakoff maintains 100%-110% pay-out ratio to reach their 7% yield. TENAGA also maintains a 120-130% payout ratio for the last few years and have been paying dividends by drawing down on borrowings. If not for the special dividend payout, TENAGA is around 5% dividend yield. As for YTL International, that one is a special one, with the highest leverage among all power concessions in Malaysia, and constantly rising borrowings.

Share Price Comparison

As we can see here, despite having superior valuations, with a steady 6% dividend yield at a very comfortable 50-60% pay-out ratio, till today RANHILL is still trading far below its IPO price of RM1.2, as well as its price at the start of the year. Since the recovery post March, it has been steadily marching downwards.

I think this is mainly due to two reasons.

- Lack of coverage by fund houses.

- Misunderstanding towards the 3-year water license (It is backed by a 30 year lease among other things like profit gurantees).

And so, to begin, we need to understand the business, which starts with the largest portion.

Understanding the Business – Water Concession

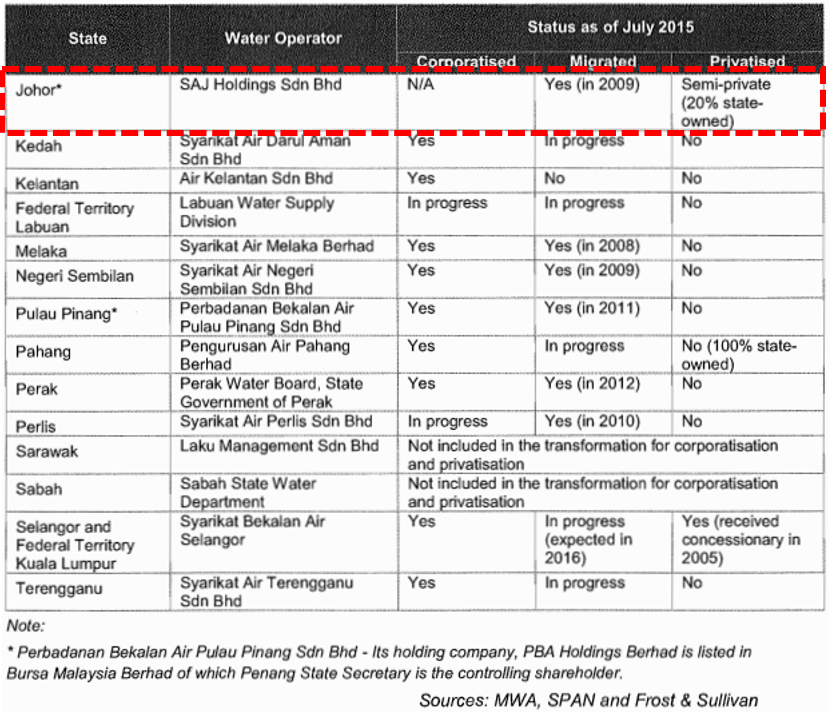

In 2006, the water concession business in Malaysia was restructured. A water asset management company known as Pengurusan Aset Air Berhad or (“PAAB”) was set up to acquire existing water infrastructure and build new water assets that will be leased to water service operators. No new water concessions will be granted, and existing concession holders was given the option to migrate to a new licensing regime, where licences are granted by the Minister of Energy, Green Technology and Water, Malaysia under the recommendation of Suruhanjaya Perkhidmatan Air Negara (“SPAN”).

This restructuring was done then, as most of the water concessions in Malaysia were severely lossmaking from being unable to raise the rates, and because of this, were naturally unwilling to invest in improving or maintaining the current water assets.

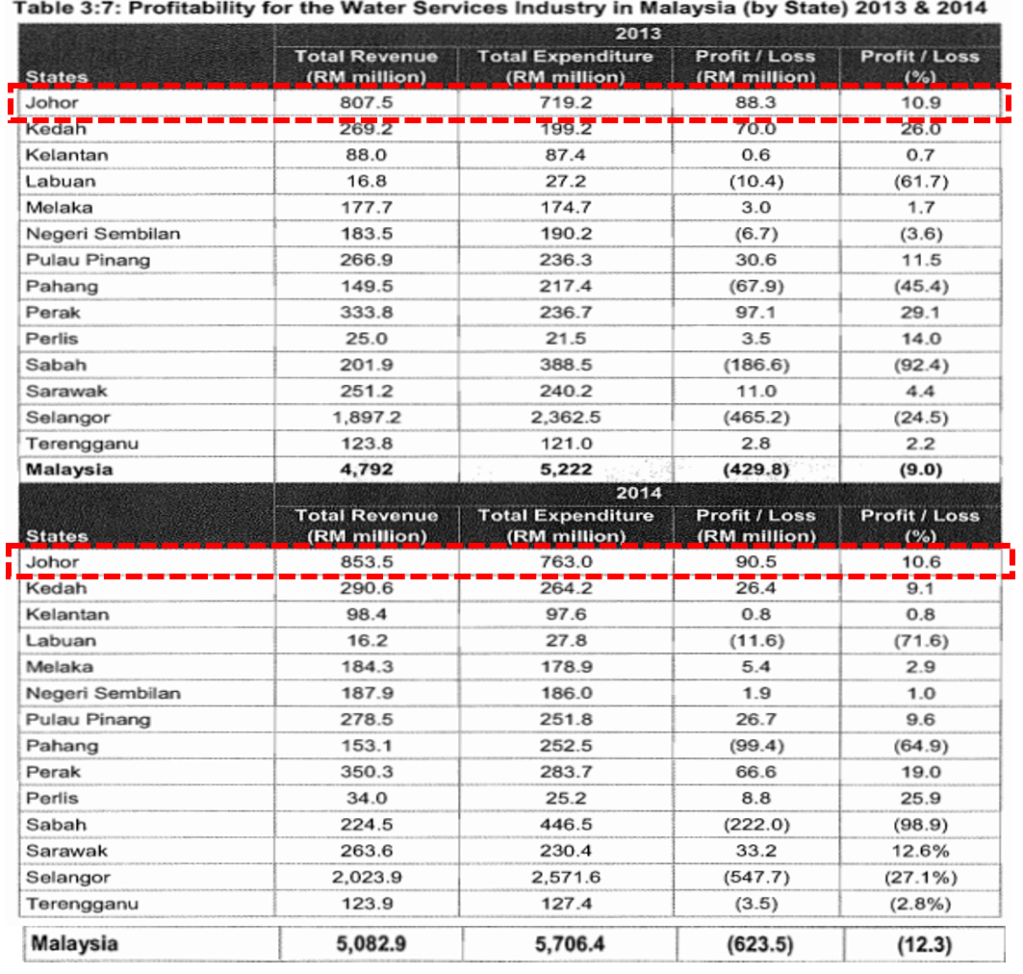

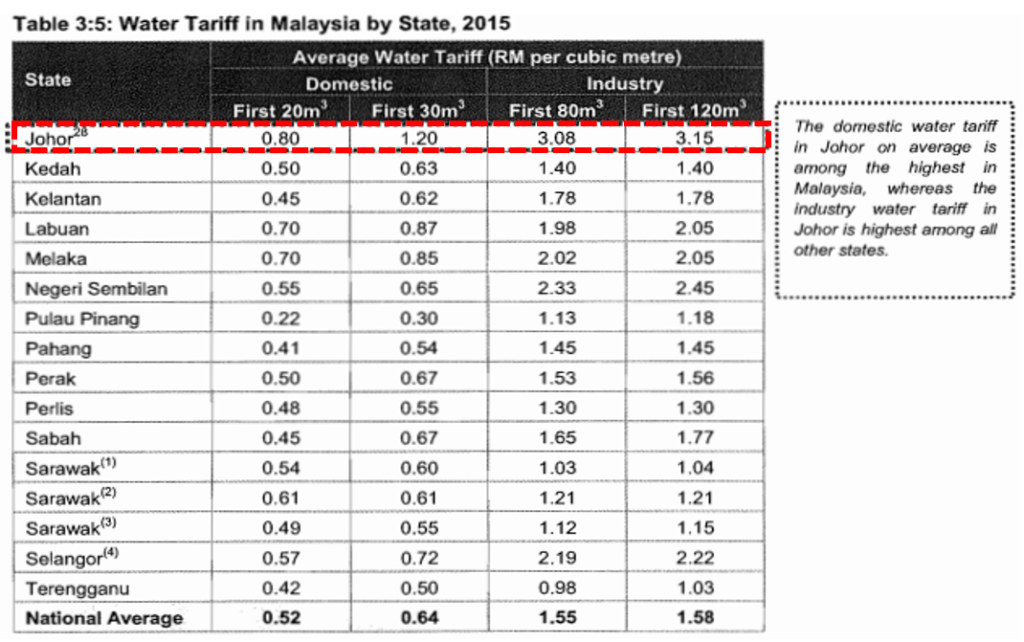

In Malaysia, the water industry as a whole is loss making. Only Johor, Pulau Pinang Kedah, Perlis, Perak and Sarawak are consistently profitable. Most of the states above are profitable mainly due to cheap raw water source.

Johor does not have a cheap water source. However, they are able be profitable as they started from a base of higher water rates, as Johor is one of these areas where water tariff increases are quite common and not politically linked.

And as Johor is the only profitable privately owned water concession other than Pulau Pinang,

The management decided to maintain ownership of their water concessions (unlike Selangor for example, where all the concessionaires were eager to sell the water concessions).

And so, during the restructuring, Ranhil did the following.

Pre Restructuring

- 30 Year Concession from Johor State Government to provide source to tap water service. Ranhill is required to continuously invest in water assets to meet the continuous demand for treated water.

Post Restructuring

- Ranhill enters into a Master Agreement with the Federal Government of Malaysia, State Government of Johor and PAAB.

- All existing water infrastructure in the State of Johor (as well as the underlying liabilities) was transferred to PAAB.

PAAB is now responsible for financing all new water infrastructure assets as when detailed in a business plan submitted every 3 years by Ranhill to Suruhanjaya Perkhidmatan Air Negara (“SPAN”). - As per agreement, Ranhill is given the right to lease all the existing and new water assets from PAAB for a period of 30 years from 1 September 2009.

- Every 3 years, Ranhill needs to apply for a license to continue providing water supply services for the state of Johor. They need to submit a business plan, which encompasses the lease payments to PAAB and the investment plan by PAAB to invest in water assets, to SPAN for approval and renewal of operating license.

Key Details of the Agreement with the Government

- A guaranteed profit after tax margin of 9%, as long as KPI’s are met If this margin is impacted due to government’s failure to increase water tariff as projected and agreed in business plan, or from increase in unit price of electricity. The government of Johor shall make good on the return, by either paying compensation, or reducing lease payments to PAAB.

- Lease payment to PAAB (the largest costs in RANHILL) is calculated by applying a formula based on the total investment outlay by PAAB in the water assets and an annual charge rate of 6%, escalating at 2.5% per year.

- Allocation of 20% shareholding to the State Government of Johor.

The essence of the above terms basically results in this being a guaranteed profit business (with the profit margin being guaranteed, not the return, this means actual return will be higher as volume increases).

And the State Government of Johor, by virtue of their 20% stake in the company would be inclined to maintain the profitability of the business.

And to prove it, we need to look at it from two perspective,

- Have the water tariffs increased over time (we assume every 3 years given that the license is renewed every 3 years)?

- If the water tariffs were not increased, did PAAB reduce its lease payments?

Guaranteed Profit – Increase in Tariffs

As we can see here, on 2015 before the IPO, Ranhill have successfully increased the tariff in 2015 after 5 years without increasing rates.

Since then, there has be no indication in terms of the rate increasing again. In which case, have there been any reduction in lease payments?

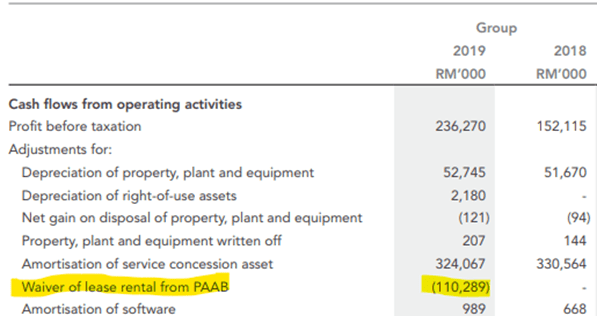

Guaranteed Profit – Reduction in Lease Payments

On 2019, there was a waiver of lease rental from PAAB of RM110.3 million, which is likely for the make good of the profit guarantee as agreed in the concession agreement.

This is a high-level summary of the water concession business financials before consolidation.

Understanding the Business – Power Concession

The water concession business is the largest contributor to the business with over an 80% share of the revenue.

The power segment contributes most of the remaining 20%.

Ranhill is the owner of two power plants in Sabah.

- RPI 1 – 190MW Teluk Salut Power Station (2029) – 80% Share

- RPI 2 – 190MW Rugading Power Station (2031) – 60% Share.

And like most regulated businesses, it generates very steady income for Ranhill.

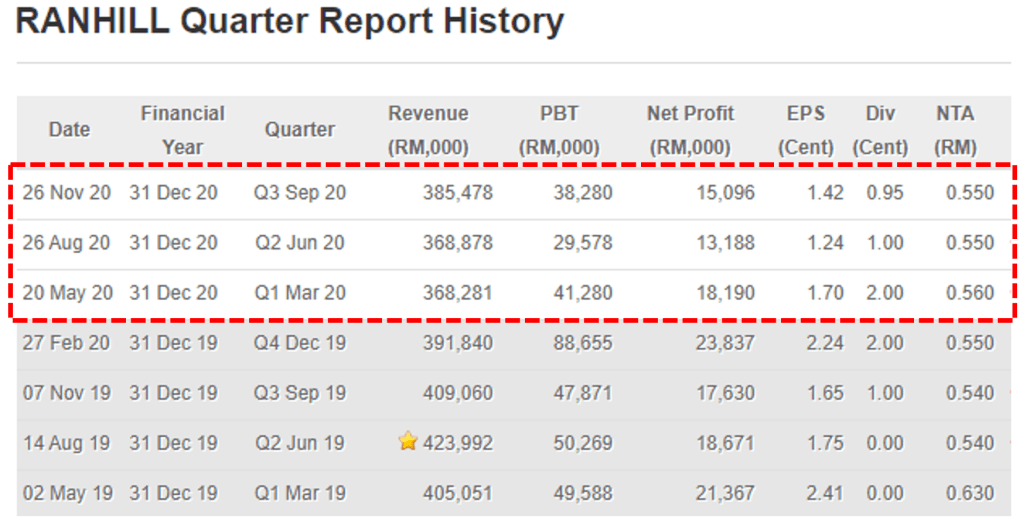

Earnings in 2019 was lower due to a scheduled hot gas path inspection maintenance work cost for GT1A at RPPI 2, which resulted in higher maintenance cost and lower revenue.

Revenue for 2019 was higher as a whole due to higher diesel costs which is passed through to the consumer.

Catalyst 1 – Water Technologies & Why Ranhill may be a front runner for the RM4bil Rasau Water Treatment Plant 2021 Tender.

What most people may not be aware of, is Ranhill’s strong competence in the Non-Revenue Water (“NRW”) (Water Wastage basically) saving technologies.

Back in 2005, they created a NRW tracking system called “AquaSmart”, which they used to monitor NRW’s by different factors, and can be accessed by the web.

And then by focusing on all the key factors, starting with Johor, they have reduced NRW from 40% to 24.1%

Currently, in Malaysia, Ranhill in Johor has the lowest NRW per kilometere at less than 0.02 million litres per day in Malaysia, despite having the second highest length of pipes in Malaysia, and 7,000 km of pipes in Johor being asbestos cement pipes that were installed 40 years ago.

These systems have also been successful implemented all over Malaysia with the followings results.

Kedah: 2008: 50% – 2010: 21%

Melaka: Dec 2008: 35% – May 2014: 21.6%

Terengganu: October 2012: 50% – January 2014: 15%

This along with their deep experience in the EPCC of Water Treatment Plants all over the world makes me think their chances of getting the RM4bil Sungai Rasau Water Treatment Plant is fairly decent.

Catalyst 2 – Revisiting Tawau Geothemal Projects & Water Supply in Indonesia

1-2 years ago, Ranhill had participated in the Tawau geothermal project (via Ranhill’s 27% stake in Tawau Green Energy Sdn Bhd) which entailed a capacity of 30MW. However, one of the partners had financial problems leading to development problems. The project was then terminated by MESTECC in 2018, and any investment impaired in 2018.

In line with Ranhill’s renewed focus into Renewable Energy Sources via LSS4 etc, any restarting of the project will be a positive.

In addition, Ranhill had also formed a consortium with several strategic partners to bid for the development of a source-to-tap project for 5 regions in Indonesia namely DKI Jakarta, Bekasi City, Bekasi Regency, Karawang Regency and Bogor Regency involving potential gross capacity of ~860mld.

Feasibility studies have been submitted to the authorities and is awaiting the outcome and approval, before a bidding process is launched, potentially in 1H21.

This project if obtained will expand its existing source-to-tap water capacity (which is currently mainly in state of Johor) by over 40%.

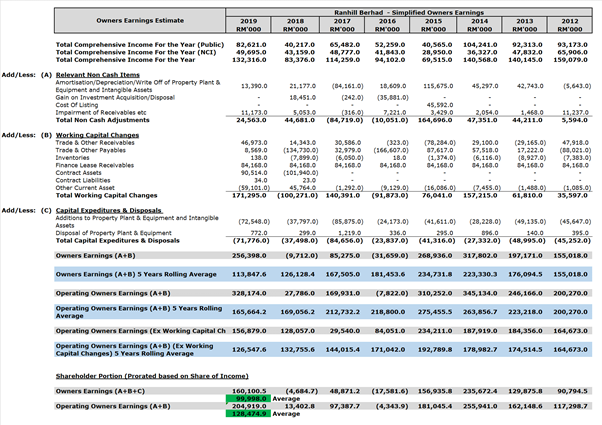

Estimates

Historically, Ranhill have recorded Owners Earnings (which includes capital expenditures) of RM100m per year and Operating Owners Earnings of RM128.5m per year.

Due to the occasionally lumpy earnings, which is mainly due to the adjustment on lease rentals which need to be negotiated, as well as the recent repair works related to the power plants in Sabah (due to strong power growth in Sabah, which resulted in power plants needing to stay operational longer than usual), the share price of the company have been volatile in the last two years.

Currently, the company is selling at the bottom end of the curve.

Given the current market capitalization of RM940m, this translates to around 10X Owners’ earnings. This is significantly lower than the market average of 15x.

At 15x earnings, Ranhill’s current value is estimated at RM1.5

And of course, this does not include the potential upsides, such as

- RM4bil Rasau Water Treatment Plant;

- New NRW projects in Malaysia;

- Success of LSS4 tenders;

- Potential Geothermal Project in Tawau, and Source to Tap Water supply tender in Indonesia.

Risk reward appears to be asymmetric as even if those wins do not materialize, one will have a profit guaranteed business at 10 times owners earnings with 6% dividend yield. But if those upsides happens, valuations will naturally go upwards.

And, One Last Thing.

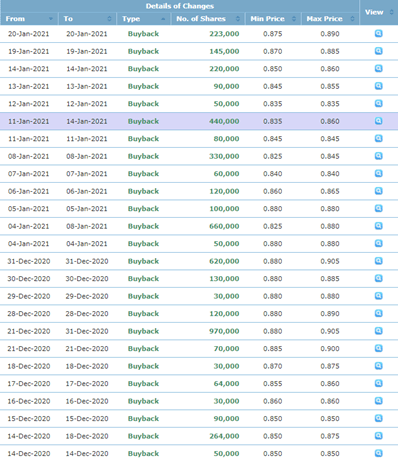

For the last year, in view of COVID 19 etc, the share price has been falling. However, there has since been spurts of buying interest in December 2020 and January 2021, as people note the recovery.

During this pandemic, given the travelling ban between Singapore and Malaysia, water usage in Johor have fallen. However, despite this, earnings have still stayed relatively steady.

In addition, since the start of the pandemic, the company have been buying back shares every other day, and for the year, have repurchased 8.9 million shares from RM0.8 to RM1.05 and they have been doing so all the way through January 2021. Providing a kind of bottom for the share price.

Very informative article. Good to see more.

LikeLike