Publish date: Sun, 31 Dec 2017, 04:33 AM

Note: The pictures in this blog didnt come out right, refer to this link for the spreadsheet of the pictures, or open the pictures in a new tab.

https://docs.google.com/spreadsheets/d/1m-TarfVVci6X7GjnovZ1-J59ac2u8xnwZCmx-EcOWOE/edit?usp=sharing

Introduction

In general, most companies fall into 3 categories when it comes to valuations. They are

- Any company other than those in the other 2 category.

- Banks and Non Deposit Taking Financial Institutions.

- Insurance companies.

For companies in category one, one can pretty much use the full spectrum of quantitative analytical tools. P/E, EV/EBIT, EV/EBITDA, EV/FCF, DCF. Can count until the cows come home if you want.

For banks and insurance companies however, you need different tools.

Insurance companies is easily the most complicated one. There is “Combined Ratio”, “Insurance Float” and “Cost of Float”. All of which you need to slowly extract one by one from the annual reports, and that’s why most screeners do not show it.

Personally, I’ve not had the time or motivation to really look at it yet. As this article will be about the valuations of banks, i won’t be going any further on insurance companies.

I will however state that, out of all the listed insurance companies in Malaysia, only TUNEPRO and LPI actually make consistently money on the premiums. Every other company loses money on the premium, but make it back via investment income. I don’t hold shares in either, but feel free to study further.

Ok, lets now start with how to value banks and non deposit taking financial institutions.

Why is bank valuations different?

Whats wrong with P/E

Well, you can, but banks have a very interesting relationship with P/E.

The thing about banks is that their business consist wholly of cash, their product is cash, their asset is the cash they borrow people, and their liabilities is the cash people borrow them or deposit with them.

This means that it would be incredibly foolish to pay, for example, 30 P/E for a bank. As they are all in saturated markets, making it impossible to grow quickly, unless one were to take on risky derivatives, or loan out money not caring about the borrower’s ability to repay.

It is also not possible leverage up quickly via deposits without severely affecting cost of capital, as higher deposit rates are required. Banks in Malaysia are already at the edge with something like 0.9-1.7% net interest margin.

Nor is it possible to source too much funds from the bond markets. First off, bond funding is usually more expensive than deposits, and banking is all about management of cashflow.

Bonds often have covenants that may result in instant recall, thereby really screwing over your cash flow, it is also not easy to structure your bond to fit your cashflow schedule and requirements.

What i’m trying to say is, banks will find it close to impossible to record the double digits growth needed to justify P/E’s above 15 due to the saturated markets, they may try to rack up the leverage or risk they are willing to bear to get that higher earnings, but that is also very difficult as banks are very tightly regulated.

Even if they were not tightly regulated, the higher the risk/leverage they are willing to bear, the higher the probability of bankruptcy. Yes, you make more short term wise, but it’s easier to go bankrupt, and these 2 set off against each other valuation wise (logically, but markets are not logical).

The only exception is when kitchen sinking is being done, so there is a depression of earnings beforehand, keeping valuations down. Like MBSB. Except in MBSB’s case, where valuations are not really down either.

Funny story.

Early 2007, Warren Buffet was one of the biggest shareholders of the bank “Fannie Mae”. When the CEO said that the bank were targeting for double digit growth in revenue and profit, Warren immediately started dumping the stock and was completely out by 2008.

The company, using CDO’s and derivatives, as well as increased leverage, met its target of double digit growth in 2008. It also went bankrupt during the financial crisis of 2008 and was one of the banks bought out by the government to prevent a meltdown in the financial markets.

How about EV/EBIT?

Also known as earnings yield, or as Joel Greenblatt likes to call it, the magic formula that beats the market (Do note it beat the market then, now that everyone knows and since markets are a dynamic environment, that statement may no longer hold true moving forward).

What is EV or Enterprise Value? EV is the real cost of the company if you were to buy outright. In essence it is:

Enterprise Value = Market Capitalization + Borrowings + Minority Interest – Cash and Cash equivalents.

Except in banks, all their liabilities is borrowings, and all their asset is cash and cash equivalents. Do the calculation and you basically get back your Equity.

How about EBIT? Also known as Earnings before Interest and Tax.

All your expense is interest expense and all your earning is interest income wor. Habis. Count so hard, get back zero. Again irrelevant.

How to Value?

Banks are incredibly complex, with multiple products and segments etc etc. It is close to impossible to do a proper detailed analysis even if you’re the analyst covering it. The only time a proper one is done, is when there is a M&A going on.

However, this does not mean it is impossible. We can still do a rough, rule of thumb valuation. How?

Let’s try asking warren buffet.

“Well, a bank that earns 1.3% or 1.4% on assets is going to end up selling above tangible book value. If it’s earning 0.6% or 0.5% on asset it’s not going to sell. Book value is not key to valuing banks. Earnings are key to valuing banks. Now, it translates to book value to some extent because you’re required to hold a certain amount of tangible equity compared to the assets you have. But you’ve got banks like Wells Fargo and USB that earn very high returns on assets, and they at a good price to tangible book. You’ve got other banks … that are earning lower returns on tangible assets, and they’re going to sell — they’re going to sell for less”

“Banks are not going to earn as good a return on equity in the future as they did five years ago. Their leverage is being restrained for good reason in many cases. So, banks earn on assets but the ratio of assets to equity, the leverage they have determines what they earn on equity.”

If you lazy to read, what he is saying here is this.

For banks the key thing is a high Return on Asset (ROA), something above 1% shows that your asset is valuable and thus worth more. It does not look like much, but since most banks are very leveraged, that 1% usually translate into a much higher Return on Equity (ROE).

Your ROA is in turn linked to your book value. The higher your ROA, the more valuable your asset, and the higher the “Price to Book” (P/B) multiple people are willing to pay.

In general, an asset with a ROA of 1% should be valued at 1 times Price to Book.

Except, that’s not the end of it.

Because in investing, I’m not buying the asset, I’m buying the company. This means what I’m interested in, is the ROE not ROA.

If a bank has zero leverage, and the ROA is 1%. Using the previous rule of thumb, if I were to buy the bank at 1 times P/B, I would be buying a company with 1% ROE, and will be effectively valuing it at 100P/E, which is insane.

This means leverage is key. If the bank is leveraged 10 times instead. That 1% ROA, translates to 11% ROE. This means i’m paying a P/E of 9 times, much more reasonable.

Which gives rise to this rule of thumb. I came up with this on my own, i dont seem to read it anywhere else.

“The fair value of a bank with ROA of 1% and leverage of 10 times, is worth a multiple of 1X Book value”.

Except, it still isnt the end of it!

Because this rule of thumb does not price in the risk of bankruptcy due to leverage. And this can give rise to some pretty interesting edge cases.

One thing to note about banks is the method of recognition of liabilities and assets.

Liabilities : Marked to Cost – What the bank owe, the bank must pay. This figure is absolutely fixed and set in stone.

Assets : Marked to Market. –Whatever asset the bank has, its value depends on what the market will pay. Ie, it fluctuates. Due to leverage, if it drops low enough, a bank can go bankrupt. Similar to margin call

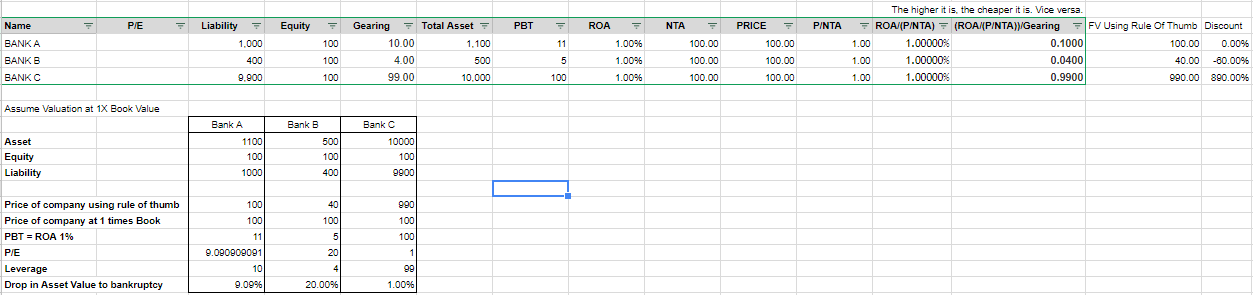

Lets Imagine Bank A, Bank B and Bank C.

Bank A

The bank has ROA of 1% and is leveraged 10 times. If an investor pays the 1X book value or RM100, he gets a company at a P/E of 9.1 and ROE of 11%. The bank is also very unlikely to go bankrupt as asset values would need to fall 10%, which is very unlikely. Pretty fair deal.

Bank B

Bank B is exactly the same as Bank A, except it is only leveraged 4 times instead of 10 times. In this case, using the rule of thumb to calculate fair value, the fair value of the bank is only RM40 despite book value being RM100, with the same exact level of quality as Bank A’s.

For this bank to go bankrupt, asset values need to fall by at least 25%, a drop which was only almost achieved for some banks in the 2008 crisis.

Therefore, by being prudential and conservative, so much so that this bank would actually survive the 2008 crisis comfortably, the market punishes it by valuing its assets (which is just as valuable as Bank A’s) at 0.4 times book value instead of 1X.

Bank C

Now, Bank C is in every way the same as Bank A and Bank B. Except, at this bank, the CEO has got balls like Donald Trump. His balls literally clicks when he walks.

This bank has a leverage of a whopping 99 times. Absolutely insane. A mere 1% drop in asset value, and the bank will go bankrupt.

If one were to pay the book value for this bank, ie; RM100, the P/E will be 0.9. By this metric, it is even cheaper than Hengyuan that was at RM2 during the start of the year.

Therefore, using the rule of thumb fair value, this bank should be worth RM990. IE, You should pay roughly 9.9 times book value for a company that can go bankrupt tomorrow. Insane.

Now, do you know what i mean when i say the valuation of banks is very interesting, and why M&A of banks take so long, valuation is hard.

There must be a balance, a bank cannot do business as if they must survive 2008, or it would be very hard to make money. On the other hand, they also cannot go crazy and leverage up to the moon.

Pre 2008, leverage in banks was in high teens, now it has dropped to roughly 10 times. Seems pretty balanced.

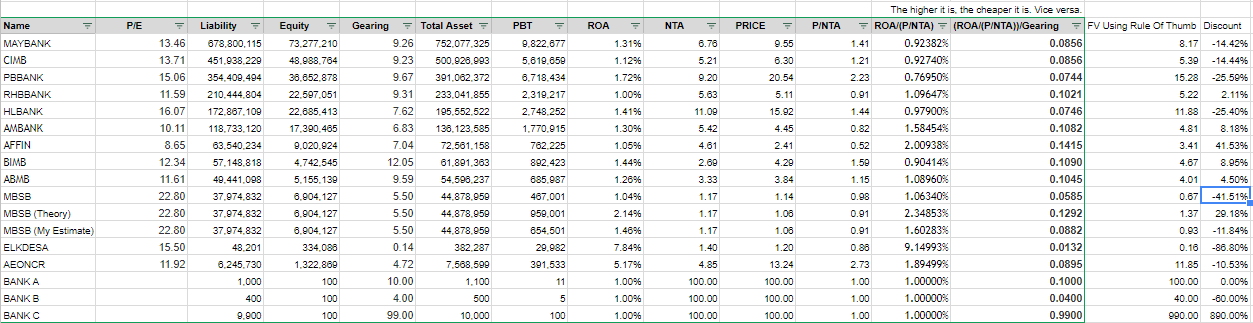

Rule of thumb table for all banks in Malaysia

As it is Christmas after all, i decided to give a present to I3 for all the information it has given to me this year.

Here is a valuation table i made for all banks in Malaysia approximately 3-4 months ago. The data is not updated, but its a fairly decent reference. Some financial institutions are not included in this table as they are my favorite. Not going to give those away for free.

Looking at this table, we can see that Affin is the most undervalued bank and Public Bank is the most highly valued bank in Malaysia. And, MBSB is by far the most overvalued one.

And for good reason, in the case of Public Bank, you are paying not just for their high quality asset (highest in Malaysia at 1.72% ROA). But also for Teh Hong Piow, the fantastic management, the amazing culture and the incredible track record.

Affin on the other hand, not that great of a bank, one of the smaller ones in Malaysia. Management is not great, and it shows, severely undervalued. Also leverage is not that high, which means, the potential is there somewhat. I hold a very small 2% position in Affin. I can’t help buying a little as it is very cheap. If it touches around RM3 given the current fundamentals, i’m out.

Other salient Qualitative points about banks as an investment

- In banks, as the product is cash and everything is cash. It is very unlikely that bad allocation of capital will be done. You will not see PPE purchases that turn out to be a waste of money, or money being spent to buy assets that are not being used and just held in the books. Capital is usually used very efficiently in the markets.

- Bank earnings are generally, more stable, and not subject to sudden upwards or downwards swings. Unless the bank loaned money to places where it shouldn’t be loaned. For example, in 2013, there was record earnings all round for banks, as the banks were loaning money left right center to oil and gas companies. Come 2014, 2015 and to an extent 2016, impairments left right center. Due to the fall in oil prices, and all these oil companies being unable to pay back the loan. Only one bank stayed out of that foolishness. The one and only Public Bank. And like clockwork, every quarter, revenue and earnings is up around 2-5%. The last time they had a red quarter (drop in earnings or revenue), was in 2008 during the peak of the financial crisis, and only once. Incredible.

Why i think Coldeye is wrong on MBSB

For the last 1-2 years, Coldeye or “Fong Siling” have been pushing MBSB as his favorite. And he has put his money where his mouth is. Coldeye holds 13,300,000 shares in MBSB or 0.23% of the company. I have no doubt this is probably his largest position at roughly RM13.8 million.

This year, one of our veteran stock pickers ICON8888 have also chosen this stock as one of his favorite for 2018.

Allow me to (arrogantly) say why i think they are making a mistake. Feel free to correct me if you feel i have made a mistake, mis-pricing whatever risk or gains, or coming at it from a wrong perspective. I too like to make money, if i’m wrong, then i’m happy, cause i can buy some now.

Looking at the table above (Look at “MBSB”), at current ROA and leverage, the fair value of MBSB is actually RM0.67 compared to the RM1.04 as at 29 December 2017. This means it has about 35% more to drop before reaching fair value.

Except, it isn’t so simple. According to management, the reason why earnings are so low, is due kitchen-sinking of impairment charges for the last 1-2 years to bring their provision standards in line with a typical bank in Malaysia.

According to management, Impairment for the last 13 quarters total RM2.14 billion. Impairment relating to the exercise amount to RM1.6 billion.

What the management is saying here, is basically, if not for the impairment exercise, our profit will be higher. By how much then. Well taking RM1.6 billion divided by the number of quarters, that is approximately RM123 mil per quarter, or RM 492 million extra in earnings.

Now, if you think this management is 100% honest, no incentive to fry up price or make themselves look good, and like god, estimates is 100% correct.

We should then add back the RM492 million into the rolling earnings (look at “MBSB (Theory)”), the fair value now shoots up to RM1.37. This means MBSB is undervalued by RM0.33 or 24% compared to current market price. Now its definitely looking like a decent buy.

Except, what the management is also telling from that statement above, is that actual operating impairment is only RM540 million for 13 quarters, which is RM39.5 million per quarter RM158 million per year.

Given that MBSB asset size is RM44.9 billion, that translates to an impairment rate of only 0.35%. For the record, Maybank’s is roughly 0.5%.

Except, here is the kicker. Out of MBSB’s RM44.9 billion net asset/loan portfolio, roughly RM22.6 billion are in the personal loan space.

As it is riskier, personal loans offer far higher effective interest rates compared to say a car loan or housing loan (Effective interest rates for personal loans are on average 20% (RCECAP and AEONCR), compared to 4-5% for a car (brand new) or housing loan). Therefore, most personal loan companies have far higher impairment rates. RCECAP for example, one of the better run personal loan companies, have an impairment rate of 1.56%.

RCECAP and MBSB are very similar companies. For both of the, loan repayments are done via salary deductions. So this should mean less non-performing loans and therefore a lower impairment rate.

With the above in mind, I think MBSB’s management estimate of the impairment rate of 0.35% is far too low.

Now, using RCECAP’s impairment rate of the personal loan portion of the portfolio and Maybank’s for the rest.

((RM22.6bil*1.56%)+(RM22.3bil*0.5))/RM44.9bil = 1.03%

MBSB’s impairment should be somewhere near 1.03%. This translates to roughly RM462.5 million per year for impairments, compared to the management estimate of RM158 million.

Plugging that into my table (refer to “MBSB(My Estimate)” the fair value of MBSB, assuming that my estimate of the future is perfect and i am god. Fair value of MBSB is only RM0.93. Ie, overpriced.

Assumptions where i could have gone wrong

For most loans, housing or motor, MBSB still takes back the money via salary deduction, so the impairment rate may very well be lower than Maybank’s.

Conclusion

Fair value for a bank is roughly 10PE. But make sure you take into account leverage. 15 times is the absolute maximum for a sane investor, most banks are at 10 times. Asset quality means more than leverage when it comes to source of earnings.

4 thoughts on “The Valuation of Financial Institutions. And why Coldeye is wrong on MBSB”