Well, the picture is self-explanatory. No prizes for guessing the “Del Luna”.

Looking at history, missing out on some major bull and goreng runs, appears to be a real talent of mine.

Lets list them out.

Construction, Technology and Petroleum Refining (2017 Bull Run)

Semiconductors and Steel (2017-2018 Bull Run)

Oil & Gas Supporting (2019 Bull Run)

FAANG & SP500 (2016 to 2019 Bull Run)

And now, the Gloves and Covid-19 (2020 Bull Run)

For some of them, I either buy way too little (less than 5%) or sold far too early. I guess some reflection is in order.

So, how do we begin? Well, I guess I’ll talk about 3 things.

- The Bull Run for Rubber Gloves.

- The Nuances of the Various Factors that really drove prices.

- Why Glove stocks are at 1X Forward PE.

(As many of you may notice by now, talking/writing is a specialty of mine, while making the decisive decision to sell some of some of my other holdings and leverage up to buy Glove Stocks, is clearly not.

And this is despite understanding the factors I’m about to explain to you, being privy to certain information’s from a Top Glove management meeting 2 weeks before results came out, as well as confirming things with my friends in Top Glove and Hartalega.

Its really a talent I tell you)

The Bull Run for Rubber Gloves

Well, if you’re one of those who are wholly unaware of what has been happening in the KLSE in terms of rubber glove companies, well, you must be one hell of an investor.

If you never really understood the meaning of “Mooning” (Here’s the “Del Luna” lol) as often used in the cryptocurrency space, well, the rubber stocks such as Supermax, Careplus and Comfort (along with their structured warrants) have risen far faster in the last month that Bitcoin etc ever did in a one month period.

Its ascension is quite literally a rocket shooting vertically towards the moon. (Again, aihhh)

Quadrupling or more in less than 1 month.

I could elaborate, but that would be the equivalent of explaining water to fish. There is quite simply no need to.

The Nuances of the Various Factors that drove Prices

- Unprecedented Level of Demand for Rubber Gloves

Not much needs to be said here, every time someone gets swabbed for a COVID 19 test, one pair of gloves will be thrown away, and this applies to even mass testing’s, house visits, contract tracing etc.

Demand became so strong, that glove companies today take a 20% deposit (this is unprecedented) on any orders made today, with delivery only happening 1 year from now (earliest).

- Structural Capacity Constraints

Unlike Personal Protective Equipment (“PPE”), Face Masks, or Sanitizers, there are some very structural constraints built into the supply for Rubber Gloves.

In the last few weeks, we would be reading news of some Tom Dick Or Harry, making all of the above items (except for Rubber Gloves) every other day.

There is that little girl helping to weave PPE (along with many other textile companies), alcohol companies that have decided to pivot and create hand sanitizers, Louis Vuitton and Razer (a computer accessory company) now produce face masks, and car companies like Ford now create ventilators.

The list goes on.

But we don’t hear news like these for gloves. Why is this the case?

Why don’t I hear rubber tappers or condom manufacturers going into glove manufacturing?

Its simple, in order to qualify for surgical gloves, you need FDA approval, a process which can take longer than a year for new companies.

In addition, in order to produce these gloves at an economical level, you need machinery and factories that can produce at least a few billion of them per year.

This means any additional capacity, can only come from the incumbents like Top Glove, Hartalega, Supermax etc

And these additional capacities can only arrive earliest by year end, with the additional supply likely to be nowhere near enough.

In the case of increasing production capacity of rubber gloves, its one of those things that just take time, no matter how much money you have to pour into it.

Like making a child, one cannot impregnate 9 women in order to have a baby born within 1 month.

- Price Increases

So limited supply, meets unprecedented demand, coupled with the inability to increase capacity quickly.

What does this mean?

Price increases for OEM surgical gloves at the rate of 5% or so PER WEEK. With own brand prices increasing by 200%-400%.

- Lower Costs

Due to the virus, demand everywhere else is much lower. Which means much lower costs for the glove companies.

Rubber Prices are down 30% from the start of the year.

Butadiene (For Nitrile Gloves) are down 50% from the start of the year.

Labour Costs is down or even as people have no other jobs to go to. Staff are also a very easy to train unlike the textile industry.

Gas prices are down still down around 40% from the start of the year due to lower demand.

- Everything else is shit.

There is a phrase in a Leonard Cohen song I quite like,

“There is no decent place to stand in a massacre.”

Well Leonard Cohen have not met rubber glove companies during a virus caused global economic shutdown.

They don’t just survive or maintain earnings, they actually thrive!

If what you’re looking for, is potential for upward price movements in the short, mid (or, at a stretch) long term, there is quite simply very little else to look at in the market today.

Even hospital revenues are technically down, as other surgeries are all down from people either delaying their surgery out of fear, or reduced by management in order to make capacity for Covid Testing.

Needless to say, whether you’re a fund manager, retailer or institutions, everyone piled into the rubber glove companies

- Record KLSE Transaction Volume, Record Retailer Participation

One thing our broker or banker friends would have noticed the last one of two months, is record draw-down of personal loans, house refinancing (a lot of them are for investment into stocks according to a friend at RinggitPlus) and new account creation for new brokerage accounts.

In the day for “Work From Home”, gambling/trading in stocks have proven to be a popular hobby.

Even the best of them like MPLUS is lagging a little, with Maybank’s brokerage accounts being close to unusable.

In any event, these new retail participants are more than able observe the meteoric rise of the rubber glove companies, and are certainly more than capable of doing first level analysis of the business and share prices.

And thus, we have today. Share price increases of 5X or more for some of the companies.

Why Glove Stocks are at 10 forward PE

Now, the answer behind the clickbait title.

Many of you may be wondering, he siao liao?

Heart pain until don’t know how to read already?

Isn’t Supermax etc all more than 70PE?

Well, quick question.

What happens to the bottom-line when increase in revenue is due to Margin Expansion versus Increase in Volume?

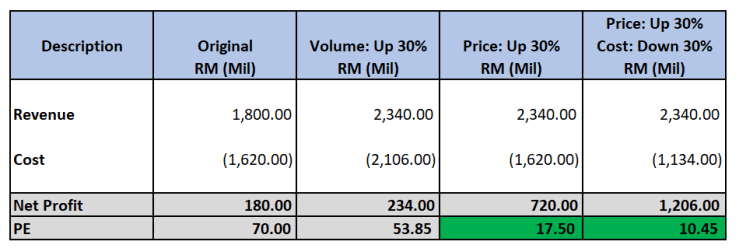

Lets do a very high level analysis with SUPERMX’s numbers.

And there you go, 10PE. A real bargain (depending on how you look at it).

So, what is the market pricing in now for Glove Stocks?

Well, the market is basically saying that COVID 19 and its other mutations will be with us for the next 2-5 years at minimum, and that demand for everything will be low, except for rubber gloves and a few other select industries.

A stagflation or depression basically.

Well, if you think that is the case, it may even be at a slight discount.

Again, do note “Target Price” and “Intrinsic Value” are two very different things.

Conclusion

Personally, I do wonder how i failed properly identify and consider the above factors. The information is all there and i even gave some thought to it in March.

How did i airball so badly and fail to purchase even 5% for myself?

Well, after some consideration, i think the main reason for it is that i tend to instantly discount/ignore stocks that are rising, especially if they are popular and Koon Yew Yin is talking about it.

This has also been one of the fundamental reasons why it took me so long to buy companies like Google, Facebook, or even the SP500 index/ Investing Overseas.

And so, by error of omission instead of commission (the favorite excuse of every value investor when he fails) , here goes another fortune slipping from my fingers.

Aihhhhh. Oh well, at least I’m still young.

Additional Anecdote

In the week before the quarterly results, me and an acquaintance (he is a trader) were discussing on glove companies and the above 10PE scenario.

We were discussing it as a trade, and this excerpt of our conversation was quite illuminating for me.

Choivo: Well, it looks like the market is not pricing in the fact that earnings may be double or quadruple. There appears to be a significant enough gap. So, what’s your trading plan? I think i may actually put 20% on it.

Acquaintance: Well, buy up to about 30% of portfolio over the next few days.

Choivo: Are you sticking to the 10% Cut loss?

Acquaintance: Yes. Gambling must have a cut loss.

Choivo: You know, I’m curious, is it even possible for you to be an investor?

Acquaintance: You know, i don’t think so. If prices drop by 10%, I cannot tahan and will cut loss instantly. In addition, if price does not move up within one or two days, I also cannot tahan and will cut straight.

Choivo: I wonder, if market drop 10% the next day, despite how right this thesis sounds, would you still cut?

Acquaintance: Yes. I will cut. If price drops 10%, it means market is telling me I’m wrong, so I will cut.

Choivo: And if it goes up 5% after it drops?

Acquaintance: I will buy back straight away.

Choivo: Why?

Acquaintance: Because Market is always right. Market is telling me now that my rule in that case was wrong, and I should not have cut loss, so i will buy back. I have no problems chasing back.

Choivo: And if it keeps doing that?

Acquaintance: Well, I’ll keep doing it, key thing is to minimize the loss and maximize the gain. If it’s going up, I won’t cut, unless I think everyone is way too happy, and everything that I know, the public also know.

Choivo: You know, I really wish I was your broker.

You know, one thing i did last year was to read the entire Market Wizard series on Traders. I can definitely see some niche that i think i am capable of doing.

However, I do wonder if its possible for me to buy something for more than its worth, in order to sell it to someone for a higher price.

Ie: Buy High and Sell Higher.

I’m not sure if I was capable of buying it at RM4.6.

But, in any event, I should have been more than capable of reading into the situation enough to buy a 10% – 15% position when Supermax was RM1.5 or so.

Oh well, you live you learn. I hope it sticks this time.

1 thought on “Ragret Del Luna: 10 PE Glove Companies (SUPERMX – 7106)”