Dear Fund Unit Investors/IOU Holders,

General Comments

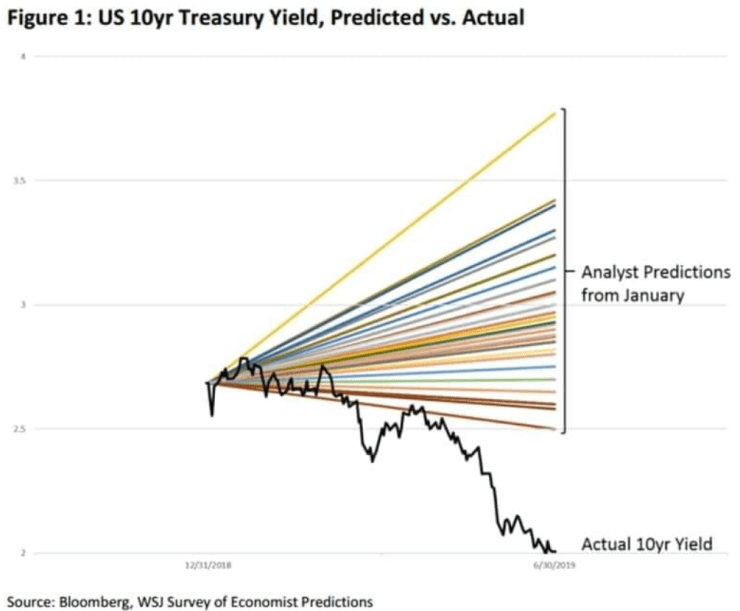

In last years letter updating all partners, I spoke a little (individuals with elephant like memories will disagree on the adjective used) on US debt, as well as how the US Government may face increasing difficulties in selling US Treasuries to fund this debt without increasing interest rates.

I ended my comments then with,

“Who will save the US if the US can no longer save itself by selling debt at extremely cheap rates?

What would happen if countries and people stop believing in the US’s ability to pay back its debt and back its currency?”

hereby implicitly expecting increasing interest rates for the US, and then this happened.

The interest rates on US Treasuries decided to take a nosedive instead, with demand of US Treasuries going up as well, when the Federal Reserve decided to inject more liquidity into the money market funds.

There are some topics (like this one) so complex and opaque, that one needs to be highly educated and well versed in the subject, in order to be unclear about the conclusions and be unable to come to an opinion.

Your highly opinionated fund manager is clearly not one of those highly educated individuals who are well versed in that subject.

When even individuals such as Howard Marks, says “I can’t. I don’t know anything about them.”, i should probably hold my horses.

Thankfully as I said in my previous letter, this is a long only, bottoms up, value-oriented fund. And as your fund manager, I do not invest based on my macroeconomic understanding and forecast but based on the value offered by the opportunities at hand.

2019 Results

In our previous letter updating our 2018 results (which was a negative, despite out-performance against the index), I wrote that:

“My continual objective in managing this fund is to achieve not just a long-term performance record superior to that of the FBMEMAS Index, but also a positive one. And unless we do achieve this, there is no reason for the existence of this fund.”

Despite the Malaysian Stock Markets “ignominy” in being the worst performing stock market in the world (with most of the other stock markets in the world hitting record highs), as well as a drop in price of our then third largest position Petron Malaysia Berhad, as of 29 December 2019, the net asset value (NAV) for each fund unit have increased from RM0.9272 to RM0.9934, an increase of RM0.0662 or 7.14%.

On the other hand, the benchmark used by the fund, the “FBMEMAS Index” which represents 98% of the market capitalization of all listed companies in Malaysia, has fallen from 11,537 to 11,431 or -0.92%.

This represents an Out-performance of 8.07% on our part against the “FBMEMAS Index” and a reason for the continued existence of this fund on my part.

Having said that, a few mistakes of omission were made this year, which could have contributed an additional 2-3% returns. And the reason for these mistakes can be summarized as thumb sucking, not setting down adequate systems and checklist when it comes to the evaluation of companies, as well as, not sticking strictly to my circle of competence.

Somewhere in this letter, I will be elaborating on these errors, and we will be rubbing my nose in my mistakes, as there is nothing like it when it comes to helping one perform better. And with everyone’s money on the line, I hope you will be thorough (and gleeful) in doing so!

Our Activities

Petron Malaysia Refining & Marketing Berhad (“Petron Malaysia”)

In my 2018 letter, I stated that,

“If anything, the bearish market of 2018, and hopefully 2019 and 2020 are very good things for those such as us, who are likely to be long term buyer of stocks. It’s very simple, lower prices allow you to buy more stock.”

Well, you may be glad to know, that the lord god does exists, and he does answers one’s prayers.

During the year, we were quite unfortunate in being unable to purchase anymore new shares in our previous top 2 positions, RCE Capital Berhad and TIME DotCom Berhad due to their prices increasing during the year by roughly 21% and 16% respectively.

However, for Petron Malaysia, the share price fell from RM6.3 to RM5.1, a fall of around 16%, while showing some improvement in the economics of the business, enabling us to increase the size of the position further.

I’ve explained this company briefly before in our previous letter, however, I do believe a more detailed explanation is due.

Petron Malaysia is a company holding both a Petrol Retail (Petrol Stations) business and a Petroleum Refinery business.

The former is a business where the government basically guarantees a profit for the mediocre, enabling those high performers to do very well, and the latter, a business that should over the long term, generate returns 2-4% above the risk-free rate, if managed well.

Since taken over by the new management (its previous owners were ESSO) in 2012, the company generated “Owners Earnings” of RM1.4 billion from 2013 to September 2019.

Excluding the require capital expenditures needed to meet the higher EURO 4 and EURO 5 requirements, the company would have generated RM2.4 billion in owner’s earnings instead.

These required capital expenditures are expected to be completed at the end of 2020, with no further significant “maintenance” capital expenditures in sight.

Despite 2019 being the most challenging year for the company thus far, with extrapolated earnings of RM200m, which is half that of 2017’s profit of RM408m, the company generated an all-time high owner’ earnings of RM602m, more than double that of 2017’s.

Even when normalized to take into account the RM390m owed by the government for fuel subsidies in 2018 that was paid in 2019. The company still generated RM212m. Incredible.

And to top it off, despite growing their Retail Petroleum market share in Malaysia from 9% in 2013, to roughly 20% in 2019, as well as, increasing sales volume from 28.8 million barrels of petrol in 2013 to 35.7 million barrels (extrapolated) in 2019.

The working capital (Working Capital consist of Trade Receivables, Trade Payables and Inventory) required to run the business since 2013, have actually dropped by RM703m or about 30%.

Imagine this, since expanding the business significantly, the management actually require 30% less working capital to run it. If this is not a sign of competent and efficient management, I don’t know what is.

And so, what is the value given to this business by Mr Market?

A business that over the long term, can churn out owners’ earnings of roughly RM200m at its cyclical low, with its average over the long term likely to be significantly higher and increasing.

At the end of 2018, Enterprise Value (Market Capitalization + Net Debt/Cash) of Petron Malaysia was approximately RM1.95 billion, or about 10 times cyclical low owners’ earnings.

Today, as at December 2019, Enterprise Value of Petron Malaysia have fallen to RM1.05b, 5 times its cyclical low owners’ earnings. (This was mainly due to the government paying the fuel subsidies owing to the company, as well as further efficiency gains in working capital.)

Talk about an absolute bargain. Since the sale of RCE Capital and the top ups during the year, this is currently our biggest position, and I am still looking to purchase more.

Here’s to hoping for further discounts in 2020.

RCE Capital Berhad

In the previous year, RCE Capital Berhad was our number 1 position, consisting of roughly 30.50% of the fund. The reasons for our purchase can be found in this article.

Lets talk about RCE CAPITAL (RCECAP)

This year in June, I sold our entire position for a profit, and the reason is as follows.

The Black Swan Hidden in RCE CAPITAL (RCECAP)

Since the time of our sale, the company’s stock price has further increased by 10%. Yes, I am that talented.

At the end of the day, I believe the gist of my decision to be correct. However, I do feel that I have made a mistaken in selling the entire position, instead of keeping say 20% of it, as the above development is only worrying due to the sheer size of the investment.

Given our governments propensity to flip flop, and shoot off its mouth without thinking things through, it does not make sense to make purchases and sales based on their comments, despite the somewhat political links this company has (it does business with politically connected entities).

All in all, this error has cost us roughly a gain of roughly 0.5%

WCE Holdings Berhad

This is a highway concessionaire company, and it was approximately 1.3% of our funds positions.

Over the last year or so, I’ve gotten relatively familiar with the Highway Industry in general, and given what I know today, I was able to better understand this company.

I realized relatively quickly that the traffic projections for the company are likely to be too high, given the change in industry dynamics.

Despite the stock rallying 40% at the start of the year, I did not sell it, betting on the market being a little more illogical and pushing it higher when sections of the highway opens.

Only in October, when the stock fell 20% below its 2018 closing price due to the finalization of a rights issue, did I sell it. This can only be attributed to a lot of thumb sucking, and not being decisive.

Me not selling at the peak or whereabouts, have cost us roughly, 0.3% to 1%. Pretty amazing for a mere 1.3% position.

Sarawak Oil Palms Berhad (“SOP”)

Some time in the end of 2017, I bought a position in SOP at RM4 per share.

When it fell to a low of RM2 per share at the end of 2018, due to

- The big hoo haa around the world on the environmental sustainability of palm oil.

- Bumper crops creating excess supply, which resulted in palm oil prices falling to a low of RM1,759 tonnes in December 2018 and a fall in SOP’s profits as well.

- Bad investment climate

In my research, I found out that Palm Oil is by far the cheapest and most efficient source of plant oil in the world (by acre) and is therefore also the most widely used.

The fact of the matter is, the sheer number of human beings living on this planet, as well as the level of resources need to support this population, is environmental unsustainable, and given this is the case, to minimize impact to the environment, our best option is to use the most efficient source available, which is palm oil.

If people were to choose to replace palm oil consumption with soy beans, canola or rapeseed, it would result in far greater destruction, as those plants require far greater acreage to produce the same amount of oil.

I then noted that the abnormally large gap in prices between palm oil and the other oils, which should result in greater demand. However, I did not top up then. Again, thumb sucking.

Instead I added more in October 2019, at RM2.4. Alas, I was again thumb sucking, and only purchased half of what I planned to buy.

It is back to RM4 today, with palm oil prices hitting a 3 year high, at RM3,000 per tonne. This is off the back of strong demand due to its previous low prices, as well as the Indonesian government requiring all diesel sold in Indonesia to have 30% palm oil content come January 2020.

Having said that, I do think that the current prices may not be sustainable, as the spreads between palm oil and soybean is extremely close today at less than 5%, which will result in customers choosing soybean instead. Natural feedbacks and all.

There is some way to go, but I feel the time at which we will dispose our position in SOP is close.

Investments in Global Stocks

A few days ago, I have informed all our partners that I have created an Interactive Brokers account, for the purpose of investing in global stocks for the fund.

To be honest, this has been a long time coming. For the past year, I have been studying a few foreign companies on and off and have noticed quite a few very interesting opportunities.

I considered purchasing the stocks through our current accounts, however, I felt this was extremely cost inefficient, with transaction fees likely to exceed 1% in many cases.

However, considering that some of the opportunities I identified, such as pork companies in china , which have since doubled or tripled their stock prices, as your fund manager, I have clearly been saving pennies while losing that potential dollars.

Having said that, I strongly believe that penny pinching is quite important over the long run, and I think with this account, we can now proceed to both pinch pennies as well as earn dollars!

In 2019, many opportunities have been found in Hong Kong, where due to the protest, the stock market have taken a bit of a beating.

However, the interesting thing is, many of the companies listed in the Hong Kong stock market actually run their businesses in china, and its business as usual with little change in their economic potential or profits. Nonetheless, their share prices have taken a beating. This represents for us a very interesting opportunity.

In addition, during the year, I have also come to the decision that I would like to focus a lot more on investing in wonderful companies at good prices, instead of taking up cyclical and net assets positions etc.

Make no mistake, these wonderful companies do exist in Malaysia. However, as they are only a few of them (since our market is quite small), they require me to be extremely concentrated, a position I am not that comfortable in, as I am all too aware of my limitations, as well as, the things I don’t know that I don’t know.

As such I would like to limit my maximum size for each major position to 10%, instead of the current 20%-30%.

In addition, in terms of the economics of a nation, I believe that a wonderful company surrounded by a big group of Chinese who are constantly looking to make more money is likely to do better than one surrounded by people who are not so inclined to do so, while beset by religious and racial problems.

Over the next year, I expect to make foreign stocks around 20% of our portfolio, with this percentage likely to increase over the years, as far more opportunities are bound to exist globally.

The Present Portfolio

| Company Name | Percentage |

| XX | 22.11% |

| XX | 16.81% |

| XX | 10.59% |

| XX | 7.20% |

| XX | 5.38% |

| XX | 4.44% |

| XX | 3.78% |

| XX | 3.42% |

| XX | 3.24% |

| XX | 2.99% |

| XX | 2.06% |

| XX | 2.02% |

| XX | 1.77% |

| XX | 1.75% |

| XX | 1.75% |

| XX | 1.70% |

| XX | 1.42% |

| XX | 1.32% |

| XX | 1.20% |

| XX | 1.09% |

| XX | 1.05% |

| XX | 1.00% |

| XX | 0.97% |

| XX | 0.93% |

| XX | 0.89% |

| XX | 0.89% |

| XX | 0.80% |

| XX | 0.63% |

| XX | 0.60% |

| XX | 0.50% |

| MARGIN LOAN | (11.92)% |

| CASH | 7.60% |

| TOTAL | 100% |

The current portfolio is relatively concentrated with the top 5 positions consisting of 62.1% of the portfolio. The top 10 positions consist of 80% of the portfolio.

Most of the top 10 are companies where a certain edge has been identified, and as the price is right, their positions are relatively large.

As for the remaining positions, they consist largely of net assets plays, where the share price is selling at roughly 50-70% discount to the assets (which have been conservatively valued), and in many cases, we are being paid to wait for the values to emerge.

Most of these positions are 2% or less, as at the end of the day, we are not liquidators nor do we have control over the operations of these companies, in addition, the timing of which these values will emerge is also unknown. Having said that, I believe a very diversified holding of these shares should result in above average returns.

That said, our preference is still wonderful companies are fair or lower prices, and over time, especially since we will now be looking at foreign stocks, these net asset positions should take up an increasingly small percentage of the fund.

As always, feel free to send me a message if you have any questions.

Overall, as your fund manager, I remain grateful for your support, and will continue working hard to continue to merit your confidence.

2 thoughts on “2019 – Fund Update”