Today, i delivered a speech at the I3 Investment Blogger Forum.

Due to time constraints, i was not able to deliver the full version.

I even opened the wrong slides which did not contain my contact information!

After the event, i had a few request to post up the speech and slides in full. Well, i was planning to do it to begin with. Warning, its very lohsoh!

============================================================================

Introduction

Good afternoon,

By way of introduction, my name is Jonathan Choi. Some of the more active members of the I3 forums here may know me as Choivo Capital or Jon Choivo, also known as that arrogant sounding young fella who is not adventurous at all.

When I first got the invite to speak at this forum, I instantly thought, “Wah, must be really cannot find anyone, until me also want”. In addition, I was also given 45 minutes, the longest time slot. They must really know I very lohsoh.

I wasn’t sure if I should accept the invite, considering how many people I may have inadvertently offended online, but I decided to do it for the reference experience.

It was then that I realized that I didn’t really know what to say or present, to our typical I3 Investor audience. As many of them are likely to be older than me, further up in their careers or as I notice in this room, retirees and are thus likely to have life experience that is far more comprehensive than mine.

There is a Chinese saying I really like, “I’ve eaten more salt than you have eaten rice”, among the Chinese community, this is a saying often used by the elders against the younger member who are no big no small. I’ve gotten it a few times, and definitely deserved it most of the time.

And I think there is a lot of truth in that saying, even if the elder person is sometimes wrong. As whatever he is wrong about, it is based off a lot more real-life experience than what the younger member may be right about, his viewpoint is therefore much more nuanced, even if it’s erroneous. At times his wrong, may even be righter that your rightness.

Therefore, I did not think it would be right for me, to arrogantly think I am worthy of standing up here and spend 45 minutes lecturing my betters. I have therefore decided to spend this time sharing my experience in investing thus far and what I have learnt from it. I hope you find some value out of it.

My Experience

I was very lucky to have been exposed to Warren Buffet, Charlie Munger and Benjamin Graham as a child. My father had a copy of “The Intelligent Investor” lying around, and I think I was around 9 or 10 years old when I picked it up and read it. Parts of it didn’t make sense to me then, I was 10 years old, but the concepts of value investing stuck in my young mind very clearly. Especially those about Mr Market and Margin of Safety.

Shortly after, I found out about Warren Buffet, who had an incredible ability to explain value investing in a manner a 10-year-old can understand. I went on to read his biography and a few books on him. It was around then that I could start talking about investments with my parents and give minor input on their portfolios. Do note, I was 10 years old, so most of the time, it was just my parents being patient and encouraging with me.

Now you would think, with this kind of investment education background, I must have saved all that stock market tuition money that most people pay and went straight to buying wonderful companies at fair prices and making a lot of money. Well that wasn’t the case, as you will shortly see, one way or another, I still found a way to be stupid and foolish.

It wasn’t until more than 15 years later, in the later half 2016, having worked for around 2 years, that I took out my savings of around RM50k (my salary and some small business and trading I used to do) and started investing it. Despite having an education in investing that many would envy, I was still incredibly foolish and made mistakes the likes of which I still couldn’t believe.

One of the first stocks I remember buying was GAMUDA-WE. I bought my first batch at RM1.35 and averaged down at RM1.30. The main reason I choose this back then was because it was recommended by a very famous trader in I3 and looking at his results for the past 5 years, I got greedy. Do note I’m not a subscriber, so my experience is likely to be very different than if I was.

During the entire period I owned it, despite studying it for a long time, I just couldn’t see why GAMUDA should be worth the RM5 or, so it was selling then, however, as that famous trader had it, and had such a wonderful track record, I thought it must be good.

I kept thinking, I must be stupid, his track record is so amazing. If this genius looking fellow buys it, and I can’t see why its worth it, I must be wrong. Better buy first and just keep studying.

As I was stupid and did not know how to size my investments, that tuition lesson, which is to do your own research from the bottom up and to only do what makes sense to yourself, cost me around RM3,000. As it turns out, me and the famous trader are fundamentally extremely different in terms of our philosophy when it comes to the stock market. What works for him will not work for me.

And back then I was an incredibly frugal person, who will think very long and hard if I should pay RM1 for an egg when ordering rice. But despite that, I could somehow spend the RM8 plus the stamp duties etc to buy and sell a stock a few times in a day, a fundamentally stupid thing to do.

In just a few months, I managed to rack up transaction cost of roughly RM3,500 on a cash only account portfolio of a mere RM50,000 and falling. And only had an additional pointless losses of RM4,000 to show.

One of my most vivid memory of the time back then was, when I told a very close friend and a current investor in my fund that, “If only I had a margin account and a higher trading limit, I would be able to average down and make money”. I sounded like a pure-bred delusional gambling addict, just unbelievably stupid.

Thankfully, despite all that, the initial teachings of Warren Buffet and Benjamin Graham still lingered on my mind and managed to convince me otherwise and limited my future losses.

I can’t help but shiver thinking of the many other new market participants like me, who unlike me , were not lucky enough to have had a decent education on investing by Warren Buffet etc at a young age. I remember a colleague of mine, who borrowed RM100k from his parents, his father is a broker by the way, to trade in the market. He lost almost 80% of it.

Charlie Munger is right, in this modern world, where people are trying to get you trade actively in the stock market, actions like that is the equivalent trying to induce a bunch of young people and retirees to start off on heroin. To be fair, brokerages etc need these kind of people, they also need to eat, but i feel there is a better way of making money.

And if someone becomes rich doing stock trading, do you think they will feel a need to write a book, go around to these talks to encourage you get rich by trading? They say things like I have a trading or investment system to teach you how to make 300 percent a year and all you must do is sign up for a 3-hour course that cost RM8,000 and I will teach you. Its very easy to make money in the market.

How likely is it a person who suddenly found a way to make 300 percent a year will be trying to sell books or teaching you how to do the same for just RM8,000? It doesn’t make sense.

In addition, in the KLSE we also have a bunch of very confident people writing articles on I3 telling you to buy this or that stock as if they they’ve got an endless supply of wonderful opportunities. These people are the equivalent of those tow truck drivers who wait for people who get into accidents by trying to extort them into using an expensive workshop.

Investing is a game of reading a lot, constantly learning and sitting there all the time and recognizing the rare opportunity when it comes and recognizing that a normal human life does not have very many. And when they do come, you need to back up the truck into it.

Anyway, back to topic, it was around that moment, which is six months in and RM10,000 or so worth of tuition fees paid, that I thought something is completely wrong.

Do I even know what I’m doing?

Do I even understand what I’m buying and how it compares to the rest of the companies in the KLSE?

I said I was a value investor, but I sure don’t feel, act or think like one.

Do I even understand value investing?

And I was lucky, some people were unfortunate enough to pay millions in tuition fees.

I decided there and then I was going to study properly. The first question I had was, investing is all about putting money in the best opportunity, but how do you know which is the best opportunity in the market?

Well, I asked that question to Warren Buffet. Or at least in a proxy manner, where an interviewer asked him that same question. He told him to read the annual reports of every single public listed company in the exchange. The interviewer said, there are more than 15,000! Warren replied, Start from A.

And so, I did that, and as the KLSE was a much smaller market than the American one, there was only 950-960 or so companies. It took me around 3 months or so to finish it. Do note I was not married and single, I had a lot of time.

The next question I asked was do you even know what value investing really is? Why are some value investors so different from another? Some diversify a lot, some concentrate very highly, and yet both had great points

I decided then to read everything about value investing. One of my favorites were from Warren Buffet and Charlie Munger. the complete annual letters of Berkshire Hathaway, his old partnership letters, transcripts for the Annual General Meetings, every single speech he ever made etc. Compared to the previous question, this took a longer time to answer, just the few items above were around 10,000 – 11,000 pages.

I just want to make clear here, that I’m not saying this to sound impressive or that it is an impressive achievement. If they were difficult and boring to read, like the IFRS Accounting standards book, it would be. But these books were very easy to consume.

Why? When someone who is very wise and smart, takes the time to answer every single one of your questions of a topic you are very interested in, in a patient, detailed, comprehensive, humorous (they are quite funny at times) and most importantly, honestly and sincerely, that feeling is incomparable at times.

I’m confident that if you had a copy as well, you wouldn’t be able to put it down. It was after I had built my base of knowledge from the greats, that I could now build on it and solidify my investment philosophy.

One of the most important and insightful things I’ve learnt during from reading those tens of thousands of pages and would like to share with you is this.

Identifying a Wonderful Company

This also happens to be title of my presentation. I also feel this is one of the hardest thing to find and understand.

Now do note I mean WONDERFUL business, not “Normal”, “Good”, or “Great” business, but a capital W, “WONDERFUL” business.

In order to know what an all CAPS “WONDERFUL” business is, we need to know what is a “Bad”, “Normal”, “Good”, “Great” and “Wonderful” business.

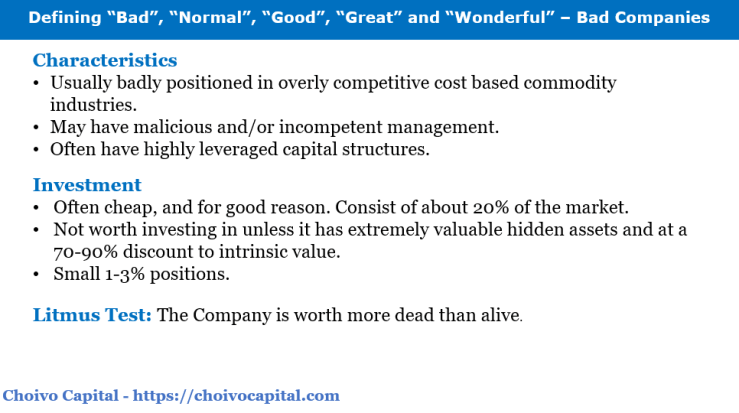

A “Bad” business, well, we all know what they look like. They are usually in overly competitive cost based commodity industries, in a bad position with higher than average cost than the competitor, may also include incompetent and malicious owners or management, coupled with horrible capital structures.

These companies are also often cheap, and for good reason. Buy a bad business for a cheap price, and another 5 quarters of losses will turn that into an expensive price.

Unless they have hidden assets that are extremely valuable and selling at minimum a 65-90% discount to Revalued Net Asset Value, and even then you should only put a small amount like 1-3% in it and diversify unless you know a catalyst event is coming. These are your Talamt, Facbind, MUI, BJCORP etc

How do you know it’s a bad business? The litmus test is this, “The company is worth more dead than alive”.

It should be noted that they are plenty of bad businesses that “appear” to be worth more alive than dead, but this is mostly illusory. From my study of the KLSE, they consist of about 25% of the KLSE.

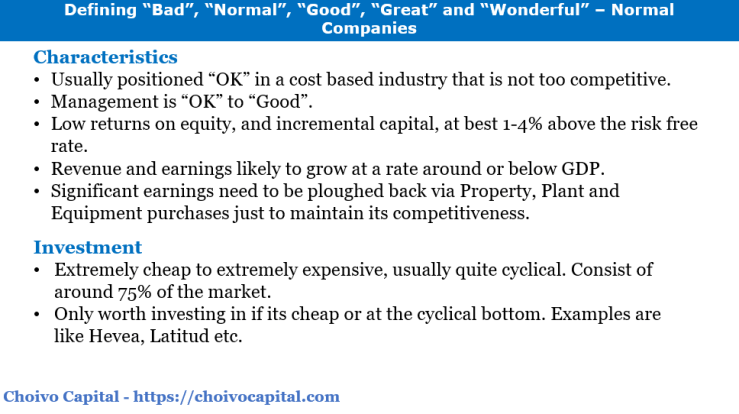

How about a “Normal” business. Well, in all sense of the word, they are well, “Normal”.

They are usually in a cost-based industry that is not stupidly competitive, management is “OK” to “Good” and somewhat shareholder-centric.

The earnings often need to plowed back to the company to maintain its competitiveness and current earnings via Property, Plant and Equipment purchases.

These companies often say they are buying new machinery to be more efficient, save cost and thus make more money and increase market share. Except they are selling a commodity and have no pricing power.

All their competitors also buy the same machine, everyone cut cost and everyone cut price, and in the end all that extra profit pass on to the customers. But not buying is also not a solution.

There is a saying, “Even if you have not bought the new machinery, you are already paying for it”

Low returns on equity and incremental capital, at best 1-4% above risk-free rate. Revenue and earnings likely to grow below country GDP.

Only worth buying is they become very cheap at the bottom of the cycle, all industries got boom and bust. You better make sure its not a permanent downturn though.

This consist of about 70% of the KLSE market. These are your HEVEA, LATITUD etc.

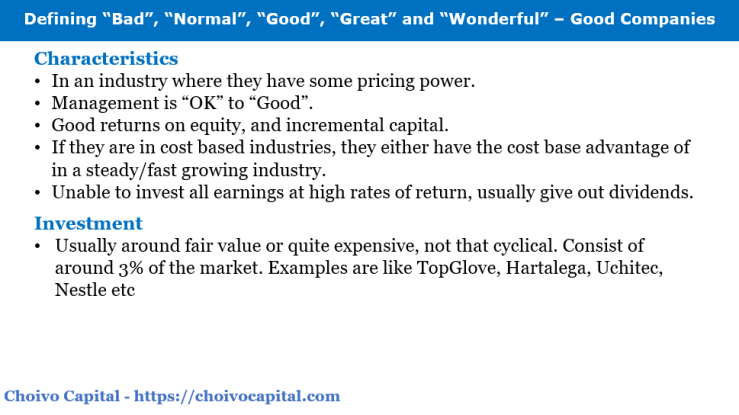

What about a “Good Business” then? These businesses are usually not in a cost centric (or at least more quality or brand centric) business, and thus have some leeway is charging higher prices.

Management is “Ok” to “Good”, these companies often have good return on equity and incremental capital.

They can also be in a cost based business, where due to various reasons, they have the cost base advantage, a little pricing power and/or is part of a fast growing industry. A rising tide lift all boats after all.

The problem with good businesses, is that they are unable to scale up, and reinvest the earnings at a high rate of return. However, if they have “Ok” to “Good” management, that do not have empire building tendencies, (If they do, you have companies like Berjaya Corporation) they will pay them out as dividends.

Having to find new ways to invest the dividends is a problem I’m sure most investors would be happy to have. This consist of about 3% of the KLSE market.

In our last two descriptions of “Normal” and “Good” businesses, you may have noticed that in both scenarios, i said that management is “Ok” to “Good”. Why do I say this? This is because whether a manager is “Ok” or “Good” in the eyes of the public, depends on the industry they are in. If you get into a horrible industry, not even the best management can save you.

For example, Tan Sri Willian Cheng is a good, hardworking and conscientious businessman, however, the industries he is in, have both had their economics destroyed in the last few years, and its almost impossible to make money. Just because PARKSON make money in the early 2000’s and to an extend 2010-2012, does that mean he was a genius then and bad business man now? I don’t think so.

Does this mean that Tan Sri Leong Hoy Kum of Mahsing or Tan Sri Jeffrey Cheah of Sunway is better than him? I don’t think so, they just happened to get into the right industry.

Is Tan Sri Ananda Krishnan and Tan Sri The Hong Piow being better than the previous 2? Or if Mark Zuckerberg, Jeff Bezos Bill Gates is better than Tan Sri Teh Hong Piow etc?

I don’t think so, it is the industry that is key, some industries are so good, that if you’re hardworking and a little smart, and get a dominant position in it and be a tycoon. That’s assuming you can find one.

There are some industries where its almost impossible to make money, if i had Tan Sri Teh Hong Piow to start a textile company in Malaysia tomorrow, the company will open on Day 1 and go bankrupt on Day 2.

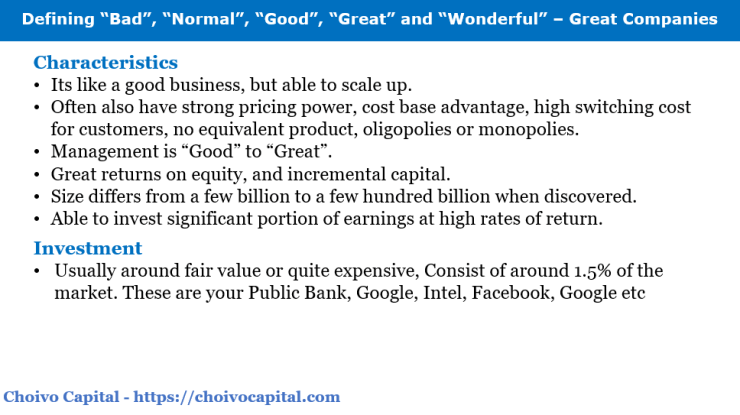

So, what is a “Great” business then? It is a good business, but with a good to great management that can scale up!

These companies can make high returns on equity and incremental capital, churn out a lot of cash, and take this money to make more at higher returns.

They vary in greatness, some can be a few billion in size, others hundreds of billion in size. In Malaysia, they consist of companies like Public Bank, Hong Leong Bank etc, overseas they are companies like Intel, Facebook, Google, Alibaba etc.

Now, you may think, those businesses are that you consider to be just “Great” seem incredible to me already.

Waseh, you telling me you so picky until even Google is not considered “Great” in your book ah? What is the difference between “Great” and “Wonderful” then?

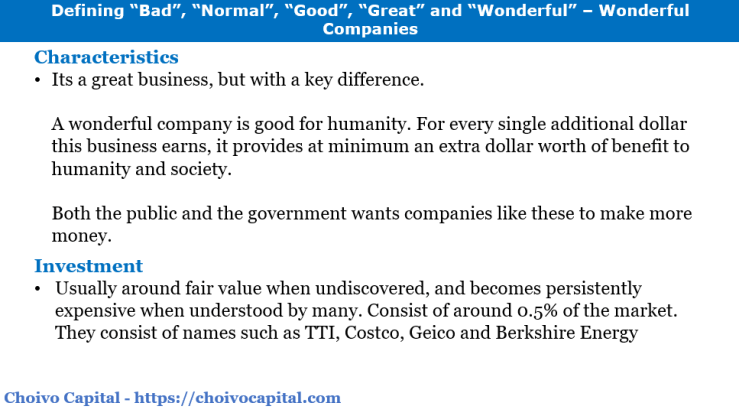

The difference is this. A wonderful company is good for humanity.

For every single dollar extra, this business, it provides at minimum an extra dollar worth of benefit to humanity and society. This kind of company, both the Public and the Government want them to make more money. If they made 1 billion today, and with the same business model made 10 billion tomorrow, the world would be better off.

Now you may think, “Make money is make money”, why is the second important, is this some kind of odd modern millennial thinking etc? Not really.

Let me give you some examples of “Great” but not “Wonderful” businesses, and why this “Wonderful/Good for Humanity” factor was important. We will start off with a foreign company first, and then we will move on to local examples.

Mainly because the foreign one is one where they were making a lot of money, and if they made more money, humanity will be even more miserable.

The Rise and Fall of Valeant Pharmaceuticals.

The name of the company is formerly called “Valeant Pharmaceuticals International Inc”. After its downfall, the company changed its name to “Bausch Health Companies Inc”.

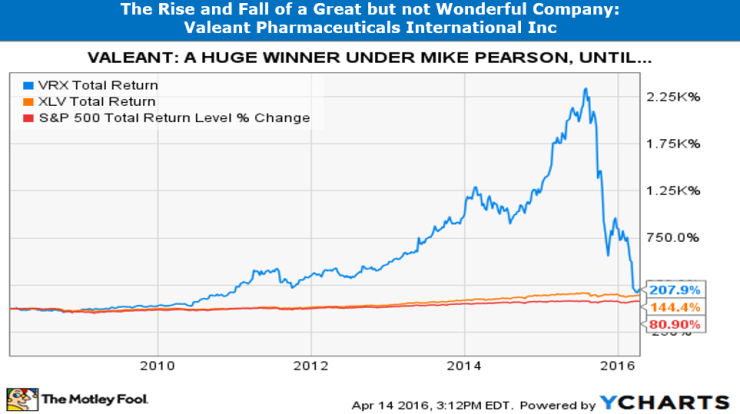

This was a pharmaceutical company listed on the Toronto Exchange. In 2008, when its then new CEO Micheal Pearson, an ex McKinsey Director with deep pharmaceutical experience, took charge. The market capitalization was less than USD2billion in 2008.

With mergers and acquisitions and soaring stock prices, it rose to a high of USD90 billion, before falling back down to a low of USD2.9 billion in 2017. A 96.7% drop from peak to trough. Its currently at USD8.2 billion.

They are a few things to note, when Micheal Pearson was hired, his was incentivized as if he joined a private equity firm. He was required personally to buy USD3 million worth of stock (he bought USD5 million).

And his compensation mainly consists of a form of restricted equity that would pay him USD4 for every USD100 in value created (measured via stock price increase), with a hurdle rate of 15%. In addition, if he hit 30%, his rewards will be doubled, and if he hit 45%, it would be tripled.

For example: Lets say Valeant was at USD2bil market capitalization, they bought another company with USD2 bil market capitalization. Total is USD4 billion capitalization. No compensation on this.

Lets say the price of the stock then went up to USD8 billion in a year. That is a 200% increase, above the 45% hurdle rate. His restricted equity at USD4 per USD100 value is now tripled to USD12. So, the difference of USD4 billion, he gets USD480 million salary that year.

Why is it important to know this, because incentives are the iron law of nature, at the end of the day you get what you incentivize for. If you put out honey, you get ants. If you put out salt, what eats salt ah? No idea.

This example also illustrates why incentivizing a CEO on share price increases is usually a stupid idea in the long term. An increase in share price does not mean the company is improving. Its better to do it via incentives on Return on Incremental Capital/ Retained Earnings not paid out.

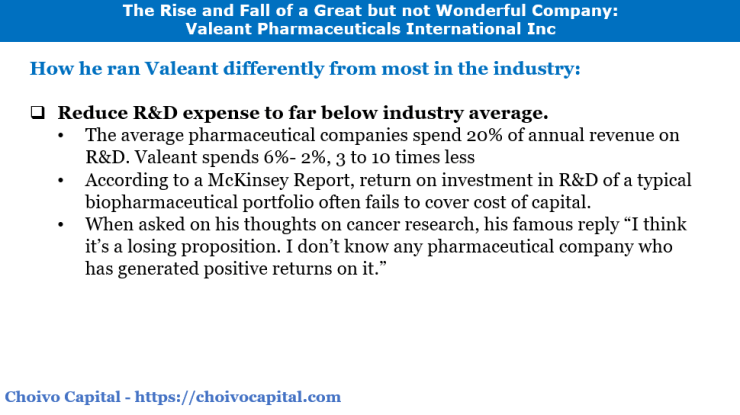

Micheal Pearson being an ex-Mckinsey Director who had deep experience in the pharmaceutical industry, did things differently from most Pharmaceutical Companies.

For most pharmaceutical companies, they way they do business, is by using the profitability of the current biopharmaceutical portfolio, to do doing research and development for new drugs.

Typically, most pharmaceutical companies spend 20% of their annual on R&D. Valeant spends 6-2% or 3 to 10 times less.

And it makes sense, according to a McKinsey Report, the return on investment in a typical biopharmaceutical portfolio often fails to cover its cost of capital, and so naturally the logical thing to do is to do less research on new drugs.

Someone once asked the CEO Michael Pearson what he thought of cancer research. He famously replied, “I think it’s a losing proposition. I don’t know any pharmaceutical company who has generated positive returns on it.”

Basically, fuck cancer research, i want my money.

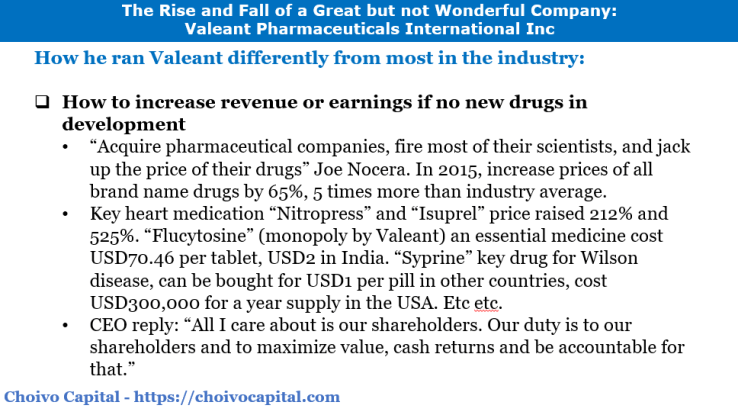

So how do they increase their revenue and profitability if they don’t have new drugs from research? It’s simple.

They bought over companies with drugs that have no easy replacements nor have generics sold in the United States. Cut their R&D cost by 80% or so, and then massively increase the prices of these drugs.

The logic is simple, like it or not, no matter the price I charge, you or the insurance company must pay for these drugs. This is one of the reasons why insurance cost in the US is one of the highest in the world.

In 2015, they raised the prices of all their brand name drugs by 65%, 5 times more than their peers. The prices of two key heart medications “Nitropress” and “Isuprel” had prices raised by 212% and 525% upon the acquisition of the right to sell these drugs.

The cost of “Flucytosine” by Valeant was 10,000% higher in the United States than in Europe, and those sold in Europe was simply not allowed to be sold in US. And here is the funniest thing, the drug was not even developed by them. It was developed in 1957, considered an essential medicine by World Health Organization’s List of Essential Medicines (therefore considered key in an effective healthcare system), and was no longer patented. However, as they were the only FDA certified generic producer, they could essentially price it as if they held the patent for it

The price of “Syprine” a key drug for Wilson’s disease, which can result in, among other things, fatal liver failure and which can be bought for USD 1 per pill in some countries, cost around USD300,000 for a year supply.

For “Syprine”, Valeant bought a pharmaceutical company called, Aton who owned the rights to sell that drug for $318 million. Despite the tiny patient base for Syprine, Valeant raised the price so strongly that they made back 2.5 times its cost in less than two years.

When Valeant acquired Salix Pharmaceuticals, the price of the diabetic drug, “Glumetza” increased by about 800%.

When asked to justify these price increases, the CEO replied, “All I care about is our shareholders. Our duty is to our shareholders and to maximize value, cash returns and be accountable for that.”

What a wonderful CEO and management.

A captive market, highly inelastic demands. Essentially, your money or your life.

What a great business.

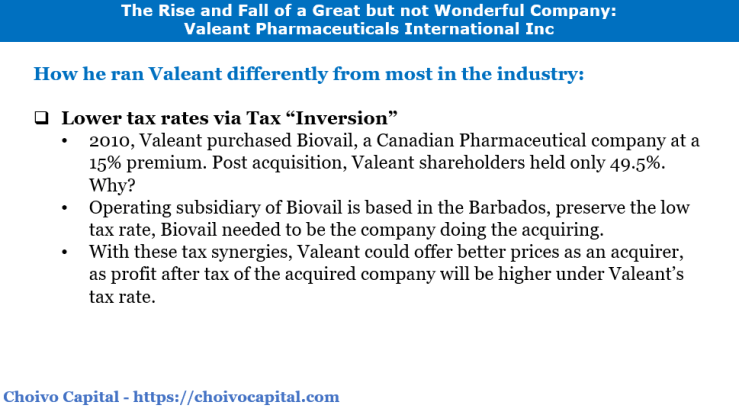

In addition, he also took advantage of lower tax rates abroad, by making tax “inversion” purchases of foreign companies.

In 2010, Valeant purchased Biovail, a Canadian Pharmaceutical company at a 15% premium. However, post-acquisition, the shareholders of Valeant held only 49.5% of the combined entity. Why?

Well, the operating subsidiary of Biovail is based in the Barbados, and to preserve its low tax rate, Biovail needed to be the company doing the acquiring.

Why was this particularly important? With the lower tax rates, Valeant could offer better prices as an acquirer.

A pharmaceutical company could be they purchased, could have a tax rate of say 38.9% (the US combined corporate tax rate) will now have a tax rate of 25%. Top that off with a couple hundred million in savings by firing your scientist and cutting your R&D budget. That’s a lot of money.

Indirectly owning a specialty pharmacy called Philidor (they created an option to buy the company that had a price of USD100million and strike price of USD0, enabling them to treat the company as if it was a third party, when the reality was anything but if) whose main business was dispensing Valeant’s drugs to consumers and getting insurers to pay for them.

Well, what happened then? Couple great business economics with a highly motivated and intelligent CEO with a lack of morality, and you get share prices rising from USD8.55 to a peak of USD257.53, or 3000% gain.

At one point, Valeant even exceeded the market capitalization of the Royal Bank of Scotland to be the company with the highest market capitalization on the Toronto Stock Exchange.

It was around the peak years of 2013, that it started becoming the darling of hedge funds and investment managers around the world. Even famous value investors like Bill Ackman (whom if you’ve read the Berkshire AGM Transcripts, you would have noticed him asking questions every other year) were investors, along with Sequoia Capital, Paulson & Co (famous for shorting mortgage bonds during the 2008 Crisis and made USD15billion in 2007, on capital of USD12.5 billion) and ValueAct whose president, Mason Morfit was quoted saying “Micheal Pearson is the best CEO I’ve ever worked with”.

It was around the peak years of 2013, that it started becoming the darling of hedge funds and investment managers around the world. Even famous value investors like Bill Ackman (whom if you’ve read the Berkshire AGM Transcripts, you would have noticed him asking questions every other year) were investors, along with Sequoia Capital, Paulson & Co (famous for shorting mortgage bonds during the 2008 Crisis and made USD15billion in 2007, on capital of USD12.5 billion) and ValueAct whose president, Mason Morfit was quoted saying “Micheal Pearson is the best CEO I’ve ever worked with”.

Even companies with friendly links to Warren Buffet such as Ruane, Cunniff & Goldfarb and personal friends and business partners such as Jorge Paolo Lemann of 3G Capital were investors.

One could scarcely find a fund manager who disagreed with Valeant or thought they were a bad investment. Except for short sellers, Warren Buffet and especially Charlie Munger who said that “Sewer is too light a word for Valeant” and that the company was deeply immoral.

We will now see how a great business, falls due to immorality. It started slowly.

First, their public failure in acquiring Allergan, which raised the Company’s Public profile, in addition to an insider trading lawsuit, as Bill Ackman of Pershing Square bought options on the shares of Allegan to help fund the acquisition and intimidate the company into selling. The fund made a profit of USD2 billion despite the failed acquisition.

During the fight, Valeant was compared very publicly to TYCO, a huge conglomerate company with a similar business model that imploded in a wave of accounting scandals in the early 2000’s. This failed acquisition was particularly painful for Valeant as their acquisition and business model required them to issue their shares, like TYCO. And with that public comparison, no board of directors would ever dare to sign as they will go to jail if found guilty.

In addition, the former of CEO of Biovail Eugene Melnyk, filed a filed a whistle-blower complaint with U.S. regulatory agencies over Valeant’s tax structure.

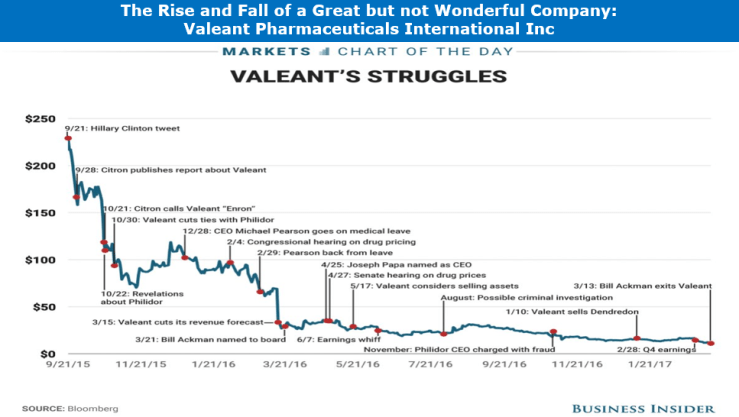

But things really took pace on 20th September 2015, when “The New York Times” wrote an article about a Martin Shkreli, a pharmaceutical CEO who hiked the price of a life saving drug by 5000% overnight.

The article mentioned Valeant, and its hiking of Nitropress and Isuprel by 525 percent and 212 percent, the day they acquired the right to sell.

The then democratic presidential candidate Hillary Clinton tweeted, “Price gouging like this in the specialty drug market is outrageous.”.

In short order, Valeant admitted that it was being investigated by both the House and the Senate, and had received subpoenas from the U.S. Attorney’s Offices, in the Southern District of New York and Boston, over its pricing of drugs and its programs to assist patients.

Its amazing how fast politicians can work, when their interest are exactly aligned with the public.

It was also around this time, that Charlie Munger made his comments on the company and research reports from various investment banks and short selling houses appeared, stating that any revenue growth was due to price increases.

The share price have now fallen to USD90 from USD257.53, in 2-3 months.

It was currently, that the final blow came, newspaper had found out about the specialty pharmacy company Philidor, and they published pieces quoting former Philidor employees who said they were told to do things such as change codes on doctors’ prescriptions to Valeant’s brand, even when much cheaper generics were available, and re-submit rejected claims by using another pharmacy’s identification number.

In addition, due to the auditors now finding out about Philidor, Valeant was not unable to file previous year’s financial report and disclosed that the S.E.C. was investigating it. In addition, the company missed its projection on a key metric by a wide margin.

On April 27 2016, Bill Ackman (Fund Manager), the CEO and CFO were forced to appear before the United States Senate Special Committee on Ageing to answer to concerns about the repercussions for patients and the health care system faced with Valeant’s business model.

After the meeting, the Senate Special Committee ordered the firing of the CEO.

It was around this time that sales started to drop as even doctors started to boycott their products whenever possible.

The share price is now USD33.36. It fell down to a low of USD8.51 on April 21 2017, amid doubts that the company will be able to service its loans. It had USD1 billion in cash and USD30 billion in loans.

Now that we’ve seen a great but not wonderful company with a lack of morality, lets look at a wonderful company.

The Wonderful Company called Costco

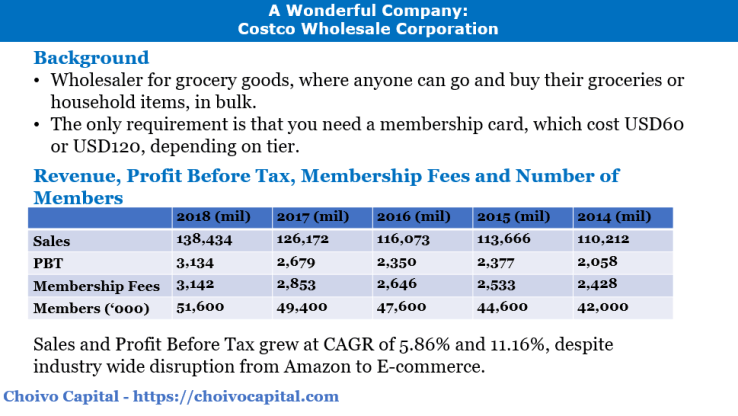

Costco Wholesale Corporation (COST) is wholesaler for grocery goods, where anyone can go and buy their groceries or household items, in bulk. The only requirement is that you need a membership card, which cost USD60 or USD120.

Here is their Revenue, Profit Before Tax, Membership Fees and Number of Members from 2014 to 2018.

Now, some of you may have noticed that unlike retail, grocery stores were not as effect by the rise of e-commerce. This is due to their margins being a lot thinner to begin with and thus more efficient and harder to run. Despite that, we still see falling sales in companies like Whole Foods etc.

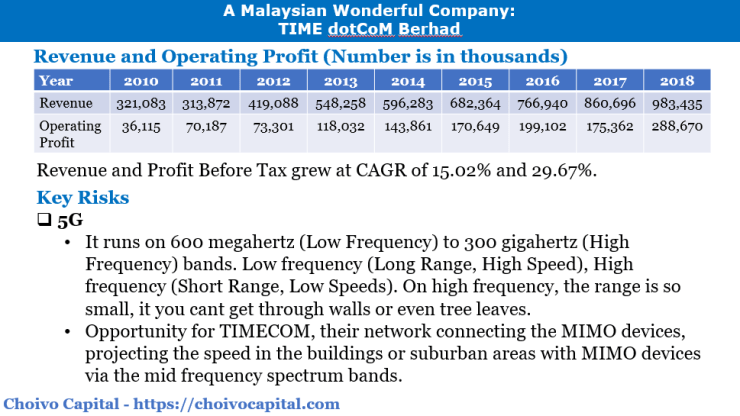

Despite this, Costco have still managed to grow sales at CAGR of 5.86% and PAT at 11.16%.

How did it do this? If you look closer, you would notice that the profit after tax of the company consist almost wholly of membership fees. They literally make around or less than zero from customers.

How did it do this? If you look closer, you would notice that the profit after tax of the company consist almost wholly of membership fees. They literally make around or less than zero from customers.

Here is what COSTCO are telling their customers. Every year, we will only make USD60-USD120 dollars in profit from you, regardless of how much you buy. You own a restaurant and spend USD20k a month? We earned USD60 from you this year. You are a big business and spent USD10 million with us? We only make a profit of USD60.

And this company by being absolutely obsessed with cutting cost, has the lowest cost base in the industry. They don’t even have name tags for the employees. They just pass you a sticker with your name, and have you wear a black shirt, pants and shoes. Buy your own.

In 2009, Coca-cola tried to increase the selling price by 3 cents per bottle, they completely refuse to stock coca cola, telling their customers,

“Costco is committed to carrying name brand merchandise at the best possible prices. At this time, Coca-Cola has not provided Costco with competitive pricing so that we may pass along the value our members deserve.”

Coca cola buckled and didn’t increase the price.

Unlike Valeant, if Costco maintained their business model and profits next year doubled from USD3.1bil to USD6.2bil. America would be rejoicing, as that would mean 51.6 million more people get to buy their daily goods and groceries for far cheaper prices.

This definitely be value accretive for the American people. The same cannot be said for Valeant.

Other Examples

This “Good for humanity” factor which results in both the Public and Government cheering for increased profits for you, is especially key.

Almost every great company that have fallen since the start of time has been due to it not being “Good for humanity”. “Good for Humanity” is as good as a moat you are ever going to get. Others fall due to fundamental technological disruption.

Why is PARKSON and SEARS etc, formerly amazingly profitable retail companies either on the verge of bankruptcy, or loss making with no end in sight?

Its simple. Back in the day PARKSON and SEARS sold household and clothing items with an extremely fat net profit margin of 20-30%, and gross margins of 50-70%

Would humanity be better of from them doubling their profits? Would humanity be better from paying double to triple for household items when it can be had for around half or a third of the price? I doubt it.

Extremely fat profit margins of great companies are opportunities for wonderful companies who kill the margins and make it up with volume, increasing the value, productivity and efficiency per dollar and per head of society.

Wonderful companies are essentially companies that increase the value of each ringgit exponentially other companies include,

Interactive Brokers – The cheapest international stock broker in the world, you can trade across most major stock markets in the world, with fees of 0.5 cents per share or a minimum of 1 dollar and a maximum of 1% of trade value. Volume discount available. For the record, this is in most cases far cheaper than what Malaysian brokers charge for buying Malaysian Stock. There is a reason why this company is not allowed to operate in KLSE.

Berkshire Energy – Unlike other energy companies with high dividend payout ratios, Warren Buffet does not require a dividend if money can be reinvested at a good rate of return. And since in America’s utility industry, the government basically guarantee you an IRR of 8-10% (most who go bankrupt here do so because they took up debt to pay dividends), the company can basically pour all their money into building the best utility plants and pipelines with no debt.

Whenever Berkshire Energy takes over another energy company or goes into a new area, energy prices drop by around 15%.

TTI – This is a global electronics parts distribution company. This is an enormously complex business where you need to manage inventories with millions of types of parts, and you make a profit of less than one tenth of a cent per part. An unbelievably hard business system to set up with close to a thousand suppliers, and the millions of data sheets for parts. Just a wonderful business.

There are some companies that appear great now, whose business is currently deteriorating due to it not being a wonderful business.

Coca Cola/Pepsi/F&N – In the last 3 years, sales volumes of soft drinks have been falling. Why is this the case? Studies have shown that sugar is almost as addictive as heroin, and it is a very refreshing drink.

Well, its not healthy and therefore not good for humanity. Would humanity be better off if they sold 2x more next year? I don’t think so.

And with the current drive to be healthier, the soft drink market is really suffering. I personally don’t really know anyone around my age group who still drinks soft drinks.

Even for our local champion F&N, sales of soft drinks have been falling, except for those of 100 PLUS, which for some reason, Malaysians think drinking 100PLUS is good for health.

I personally remember my doctor recommending me to drink it when I was younger when I had fever or stomach-ache.

Other companies such as General Mills, Kelloggs, Kraft Heinz etc is also facing falling sales.

So how many of these wonderful companies are there in KLSE. Maybe 2 or 3. There is a good chance it’s because I’m not smart enough to identify more. But it appears in line considering the size of our markets.

TIMECOM

Having gone through all the annual report of companies listed Malaysia, I managed to identify only 2 wonderful companies.

One of them had a real moat, the other appears to have a decent one. The first is around fair value or a little above fair value, the other is cheap-ish maybe.

I’m not a fan of sharing my best ideas to strangers, however, as I’ve already built up my position for the first one, and they are better opportunities in the market, and will therefore be unlikely to top up soon, I don’t particularly mind sharing this, as it will not affect myself and my fund investors much.

The main reason i gave it out back then, was because the valuation i paid was quite expensive at 25 times earnings, and as i wasn’t sure, i wanted a second opinion and for people to criticize it in order for me to find out the strength of my research.

Currently the earnings have almost doubled, without a change in the price. Personally, i’m quite happy to be paying the same price for a much improved company!

The name of the company is TIMECOM. I wrote a post on it in my website back in 2017,

An analysis of TIME dotCom Berhad (“TIME”)

However, allow me to give you just a brief overview.

The thing about wonderful companies is that when the insight comes, they are often already expensive and TIMECOM was about 10-15% above my fair value when I bought it.

I first found and understood it around April 2017, and being so excited, after thinking very deeply for 3 weeks, I sold half my portfolio and put it into TIMECOM, a little foolish.

But to be fair, I was younger, and everything else was a lot more expensive. I’ve only topped up once since then, and as my portfolio is a lot bigger now, despite not selling a share, it has fallen to around 15% of portfolio.

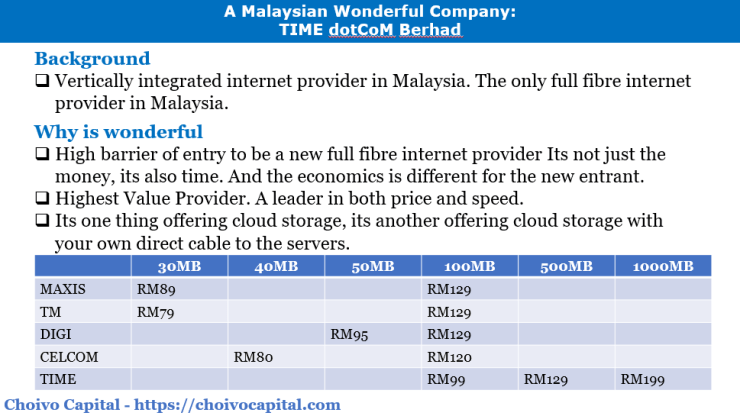

TIMECOM is the only full fibre internet provider in Malaysia and is vertically integrated with their own data centre business and shares of international underwater fibre optic cables.

Pre-2008, TIMECOM was a mediocre telecommunications company. Late 2008, they hired their new CEO Afzal. His turnaround plan was to turn TIME into a telecommunications company that connected Malaysia internally and externally with a pure fibre optic network.

They first started laying down the main backbone of the fibre network from Thailand/Penang to Johor/ Singapore in 2010, and since then, mainly provided their network services to enterprises and business such as Astro which require very high speeds and bandwidths. And in 2016, the network was finally dense enough to launch to the Retail market.

Now, why does having a full fibre network matter? Its simple, copper is inherently slower, and its signals degrade over long distances, this is not the case for fibre optic cables, as long as there is a single stretch of copper in your network line, it won’t be as fast.

And TM, has a Fibre /Copper Hybrid network, which is also why they have so many Streamyx users, who are on copper lines. This is also why TM turned extremely quiet on their TURBO plan which came out 3 days after elections. If they could sell 10x speed, they would, but they can’t, which is why 100MB is their fastest plan now.

And as we can see from the table above, they are way ahead. And if you go to my article, which was written in 2017, the gap is value is far bigger. While TM and AXIATA etc struggle with the Gorbind Singh’s pledge of double the speed at half the price, with impairments coming left right centre.

What about TIMECOM? Profits hits an all-time high, this is what you call a moat!

Now you might ask, why don’t TM or Maxis etc just build a pure fibre optic line and compete? Well, time and money. I said money second but let’s talk about that first.

TM has net borrowings of about RM15 billion, and they have a legacy copper fibre network which spans hundreds of thousands of kilometres long of km long and built over decades, replacing that is going to be expensive, especially since they still have hundreds of thousands of Streamyx users to upgrade.

It’s going to be very difficult, and TIME is net cash, and growing 18% per annum while TM sorts that out.

As for our mobile telco’s. They could, but their stocks are all very overvalued with support of a 90-100% dividend payout policy. If they drop the payout, the share price will drop like a stone, I don’t think EPF etc would find that acceptable.

In addition, they still need to buy spectrums, and build new towers, especially with 5G coming up, which already take up most of their borrowing capacity.

And to top it off, you need time. Starting in 2010, it took them 3-4 years to connect Penang to Singapore and offer to commercial users. And another 2 more years before they could start with retail customers, imagine a blood vessel, its kind of like that.

Network effects just take time, even if you have a lot of money to pour into it, it’s a little like having children, you cannot have a baby in one month by getting 9 women pregnant.

And as we can see from this table here, which strips out any one-off income, that is the effect of their moat.

When I first bought it in 2017, I expected the retail business to grow at 70-100% per annum, which translates to 15-18% growth per annum. The income and revenue did not grow at that speed in 2017, when one off depreciations, forex losses hitting the books, as well as lower IRU sales. But I could see very clearly that the recurring revenue and earnings was increasing at the pace I thought it would.

The growth and demand for their service was obvious especially if you went to their Facebook page, where people ask two questions.

- Why your installer not yet arrive!

- When you want to connect to my area

What wonderful complains to have!

It started showing the increased in earnings later mid to late 2018. The focus of the company now is in connecting condominiums. Why? Connect to one condo, you will instantly steal 200 customers from TM or Maxis.

I expanded on a few things a lot more in my article, but due to time constraints, I better skip it and go straight to the most important part risk and valuation. Feel free to read the article enclosed.

The biggest risk to this company is 5G.

Let me just give a brief layman introduction on what it is. It is the 5th generation wireless connection that runs on low frequencies and high frequency bands and is expected to be up to 100 times faster than current 4G speeds.

Now, despite how loudly people talk about the wonders of 5G, we need to note this.

4G is not even properly implemented worldwide, not in even in the US or Malaysia. Do you see the LTE sign on your phone, that stands for “Long Term Evolution”, or basically as how BN ministers use to say ”Akan cuba lah”. LTE is what you put when its not yet full 4G. You notice how they even say “Long Term”, this means few years also can mah!

Now let’s say they roll out 5G, the thing you need to know is this, it will take a long time for nationwide rollout. Because the key weakness of 5G, is that if you want to get those extremely high speeds, you need MIMO devices every 50-100m, or basically everywhere.

Those articles you read about where 5G had speed of 10-30GB per second, it’s the 5G device directly facing the MIMO device 50 meters away on the highest frequency bands. If someone walk in between, putus straight!

If they want better range, they need to use the low to mid frequency bands. SPRINT, a US company is aiming to release 5G in parts of the nation, the minimum speed they are aiming for is 2-4mb, even our “akan cuba” 4G is faster.

Now, even if they do take off in a big way, TIMECOM stands to benefit in a big way. These MIMO devices need to be connected by a fibre optic backbone, and TIMECOM is well positioned for it. And if people start using 5G for their connections, it would save TIMECOM cost when it comes to connecting to suburban areas.

When it comes to suburban areas, the reason TIMECOM does not connect to them is firstly cost, its just more profitable to connect to condo’s and secondly, because they can’t.

TM previously did not allow the use of their poles, and government does not allow above air fibre optic cables as they look ugly. And so, if TIME wanted to connect, they need to dig new tunnels to all the houses.

But if 5G took off, they can very easily just install a few MIMO devices, connected to their fibre network, near suburban areas and use the mid-spectrum bands to offer high internet speeds to homeowners.

Valuation wise, its currently 16 times earnings. A company growing earnings and revenue at 16-18% and selling at that price, translates to about 11%-12% yield. FD’s currently yield 4.6%. And to top it off, this company can really scale up with the profits they earn at good rates of return. ROE is 11%.

Up to you. Make up your own mind.

Choivo Capital

From the speech thus far, some of you may have correctly deduced that I intend to enter fund management. However, I consider it immoral for someone to manage another’s money for a fee, unless you have a high confidence level backed by a decently long track record, of your ability to obtain higher than average results.

And like a fibre optic cable network, this takes time. And so, until I get a good 5-year track record (and if I do get it), i do not do any fund management in an official capacity.

Having said that, I consider the mere act of investing to be a zero value add activity to society. A life spent getting rich by getting increasingly shrewd at buying and selling pieces of paper is a life wasted.

My main goal now therefore, is to create my own course online on investing. I intend for it to cover everything you need to know on investing and the mental models, and I also intend for it to be free.

Currently, I’ve not yet started on it, but if you go to my site and the page, I’ve listed down the list of books I believe will teach you far better than I can, and you will find my articles there, which may be interesting and of use.

At the end of the day, investing is the last real liberal art. Its about understanding human beings, business, psychology, maths, physics, economics, biology and life itself. The older you are, the more you know about life and the better you are likely to be. I’m certain that if the people in this room were as lucky as me, in being given such a good investment education, you guys are likely to be way better.

If I could help young people like me, and retirees or people advanced in their careers, understand money and investing properly, and save their tuition money, which can often exceed hundreds of thousands to millions, I think I would have lived a decent life.

1 thought on “My Speech on 2 March 2019: My experience and Identifying a wonderful company.”