Publish date:

Well, what is there left to be said about this company? Every kind of valuation has been done, with FV from RM4 to RM42.

Quarters have been predicted and failed (and succeeded once). By now, I bet quite a few members here have read enough to be armchair experts in refinery types, crack spreads, oil prices, derivatives, and forex.

Well, I think there is one thing left to be said. I don’t think anyone really asked this question.

Just how good is the refinery of Hengyuan? and, What is the real operating earnings flowing from the refinery alone?

They are a few factors that affect the profits of refineries.

- Derivative Gains/Losses (Due to oil price movements).

- Stockholding Gains/Losses (Due to oil price movements).

- Stock write down or write backs (A small factor usually).

- Impairment/Writedown on property (Small factor most of the time, but a HY got a RM461mil hit in 2014).

- Forex Gain/Loss (Can be a big deal).

- Crack Spreads (Duh)

But from what we can see the last couple months, its generally futile to try and predict short term quarters or estimate long term earning power by trying to predict crack spreads, oil prices and forex movements. They are many moving parts and thus quite complex and chaotic.

We would be better off trying to estimate the long term earning power of the company instead. At the end of the day, what is the purchase of equities other than potential earnings/cashflow of companies paid for today?

Why would I say it’s futile to predict short term results with much precision? Let’s see the following predictions.

Oil Price will go up.

This means,

Stockholding gains.

Derivative losses, as they hedge against increase in oil prices.

Compression of crack spread as there is a time lag.

Oil Price will go down.

This means,

Stockholding losses

Derivative gains, as they hedge against increase in oil prices.

Expansion of crack spread as there is a time lag.

All of these net off against each other. So often, you don’t see that much of a change. Or if you’re the kind to try and use crack spreads to predict profits. And the effects also depend on how much inventory held at that point in time, how much are covered by derivatives and at what strike price etc.

If it goes up, everyone delays maintenance, increasing supply and resulting in spreads to go down. As we clearly just saw.

If it goes down, everyone starts maintenance, lowering supply, resulting in the crack spread go increasing.

At the end of the day, you only need to know this. On average there will always be a positive spread between the net price of refined petrochemicals sold and the price of oil per barrel.

It’s impossible for the long term difference of the total price of refined goods compared to the price of oil per barrel to be less than zero.

So what is the eternal constant? What is the truth of refinery business that will not change from day to day? What can we try and find out today that will still be useful next year?

Its simple.

Just how good is your damn refinery?

How efficient is it at refining stuff?

Can it refine at a profit if crack spreads are thin? Who cares if spreads are fat, during that time, everyone also can make money. A rising tide lifts all boat.

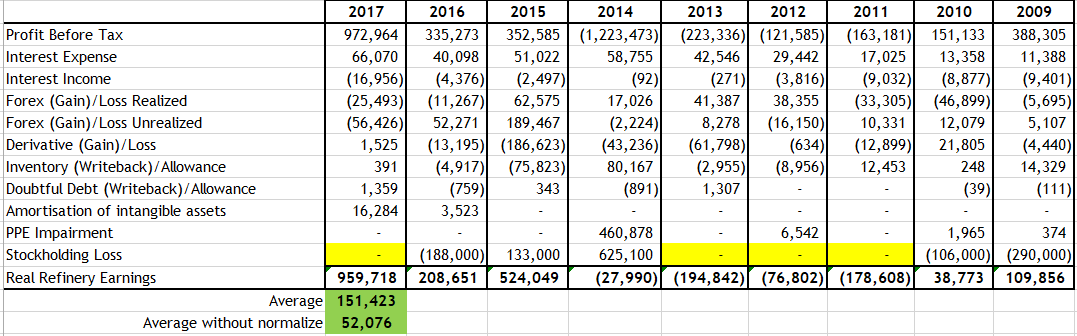

The real refinery earnings of Hengyuan.

Here is a table I created to try and to estimate the real refinery earnings of Hengyuan over 9 years. Why not 10, because I got lazy at 9. And it seems a decent enough spread between high and low oil prices etc.

I normalized the refinery earnings by removing a few items such as,

- Interest Expense

- Interest Income

- Forex (Gain)/Loss Realized

- Forex (Gain)/Loss Unrealized

- Derivative (Gain)/Loss

- Inventory (Writeback)/Allowance

- Doubtful Debt (Writeback)/Allowance

- Amortisation of intangible assets

- PPE Impairment

- Stockholding (Gain)/Loss

Which should give me a rough estimate of how capable and efficient this refinery/ refinery business is.

For the record, the PWC auditors seems to be retarded. So many figures in the cash flow seem to change from year to year. And I can’t seem to tie the unrealized forex to the “Profit/Loss Before Tax” note. Which is just weird.

So I’m probably off by a few hundred thousand to a few million each year. But if an investment needs me to be accurate to the dollar to determine its value. I probably shouldn’t be investing in it.

You don’t need to know the weight of a women to know if she’s fat, or the age of a man to know if he’s old. The value of an investment should be obvious.

I think there is a decent mix, we have 2009 to 2012 when oil prices were high, and the 2013 to 2014, during the big drop, 2015 to 2016 when there was a sustained low price, and in 2017 when oil prices shot up to 50-60 or so.

A few things to note. The main item, stock-holding losses, I was unable to find that amount for a couple of years. It wasn’t disclosed. But I think it evens out, as even if it was a loss from 2011 to 2013, the gain from 2017’s should be large enough to cover it.

If 2011 to 2013 was a gain, it’s for the better anyway. It’s better to err on the side of caution. But I suspect it wasn’t disclosed then as i wasn’t that material then as oil prices were relatively stable.

Assuming we use the normalized earnings at RM150 mil per year, Hengyuan is the trading at 19 times earnings. Do note its worse for the un-equalised one as that is only RM52 mil per year.

But that’s not the complete story

Other salient points.

- The refinery made losses last time as they had to sell to Shell at a low price.

For some reason, everyone keeps saying this, but for the life of me, I can’t find it anywhere in any of the annual reports. Nowhere does it say that Hengyuan used to sell petrochemicals to shell at a discount.

I think this is just one of those things that appeared in an OTB newsletter and everyone just took it as the truth.

In addition, even if it were true, you cannot price it too low. There’s something called transfer pricing documents, which ensure that you cannot move profits to a lower corporate tax company too much. Basically you need to sell at arms length price.

But if this is really true and material. We can expect some resilience in the earnings moving forward. But nobody says they cannot sell to the new mother company at a discount too. But would not make sense as Corporate tax rate in China is 25%, Malaysia’s is 24%.

- You cannot make your earnings pretty without additional cost.

If a company tries to make their earnings beautiful, by hedging their spreads, forex, and oil prices. They will probably incur significant cost. Options are not free. Covering your downside cost you money.

I have no idea why PETCHEM earnings are so beautiful though. Tell me if you know why!

- RM750mil upgrade will increase production by 20%.

Do you know how many time they bought PPE worth more than 500m in the last 10 years. Quite often. And as we can see they can actually make refinery losses. This could mean your losses increase by 20%.

- Plan to venture into petrochemicals trading.

Don’t forget, can make money, can also make losses. Is this their core capability. Trading and running a business is a completey different game. You want to fight with VITOL? One of the many companies that focus on trading energy commodities. They do this for a living, you’re doing this on the side.

How good is VITOL? They are one of the biggest despite being privately held. No need outside money. That’s how much money they make and how good they are.

- IMO 2020.

No comment, too far into the future. If everyone sees this a threat, won’t everyone upgrade their refineries? In which case, wouldn’t your advantage hilang d?

Conclusion.

I’ll probably just hold my 2% position. It was at 3% when i re-buy in at RM14.3 after selling everything at RM17. I think its a decent punt.

But as an investment, i don’t think i know enough about it, nor is the value so obvious that its a no brainer.

Good luck everyone.

Also let me know if i missed out on anything, or am wrong about something.

No point having an ego in the market. If i’m wrong, let me know, so that i can buy more and make money too!