Publish date:

WCE Berhad has always been one of the companies I have always been interested in. And one of the main reason, is because an investor whose thought process i trust, keeps talking about it. That person is of course, “Felicity”.

However, I couldn’t really place a value on it beyond, “Yeap, from the feel of things, it looks like it’s going to be very valuable, or is very valuable already”.

However, a few days ago, i decided to properly do a DCF valuation of WCEHB, and what I saw helped me understand why felicity and so many other large investors like the Pang’s (Mamee) are willing to hold that stock through lower and lower fund placements and zero positive price movements.

Here is my brief analysis and valuation of WCEHB.

Introduction.

Whatever background info you need to know about WCEHB is already written down by felicity here.

http://www.intellecpoint.com/search/label/WCE

However, here is a brief overview.

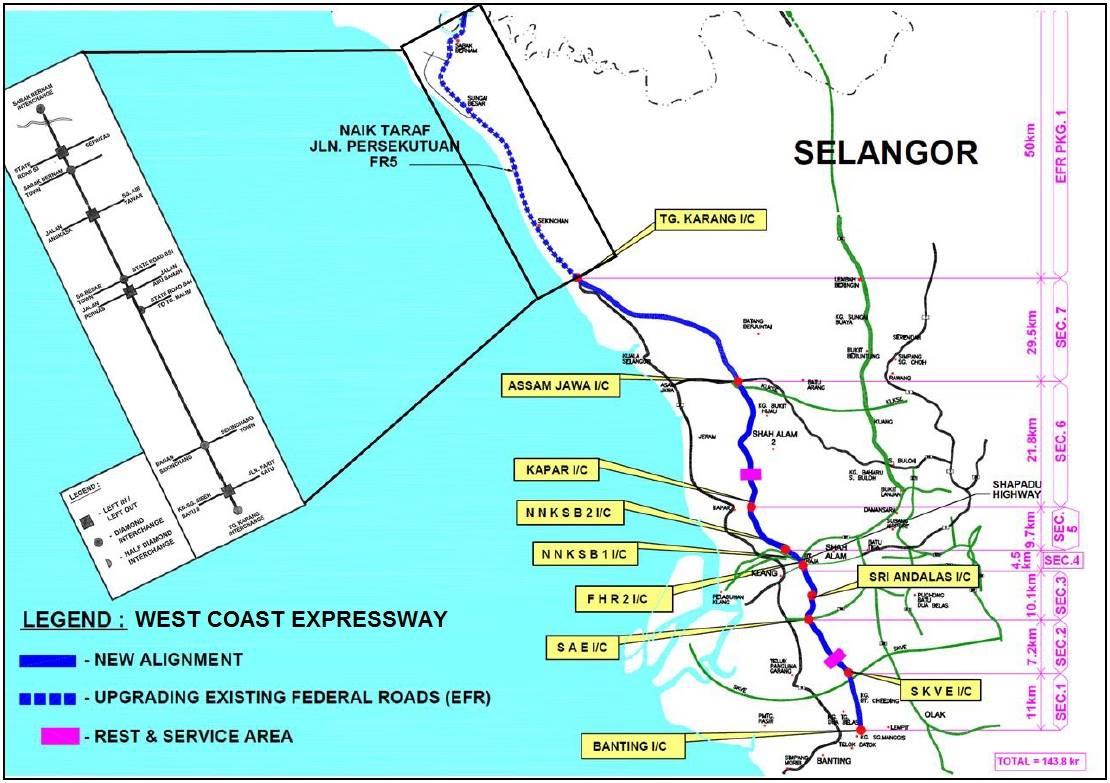

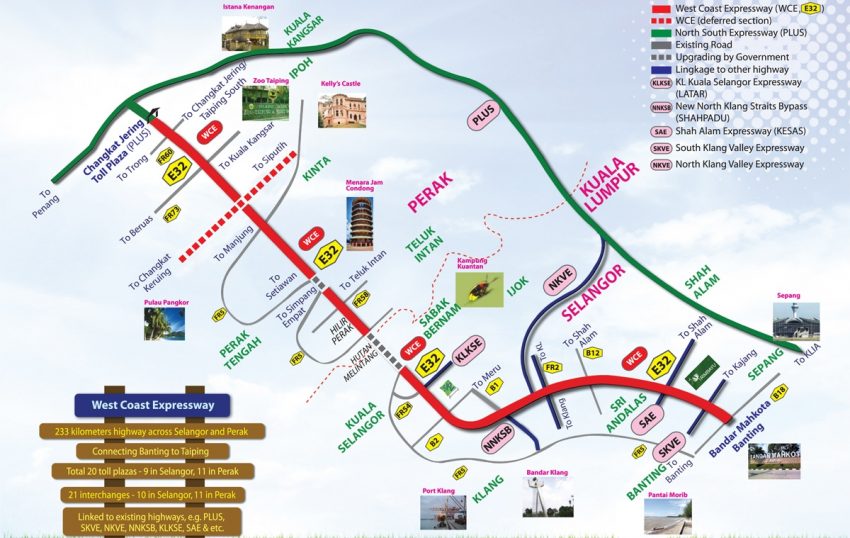

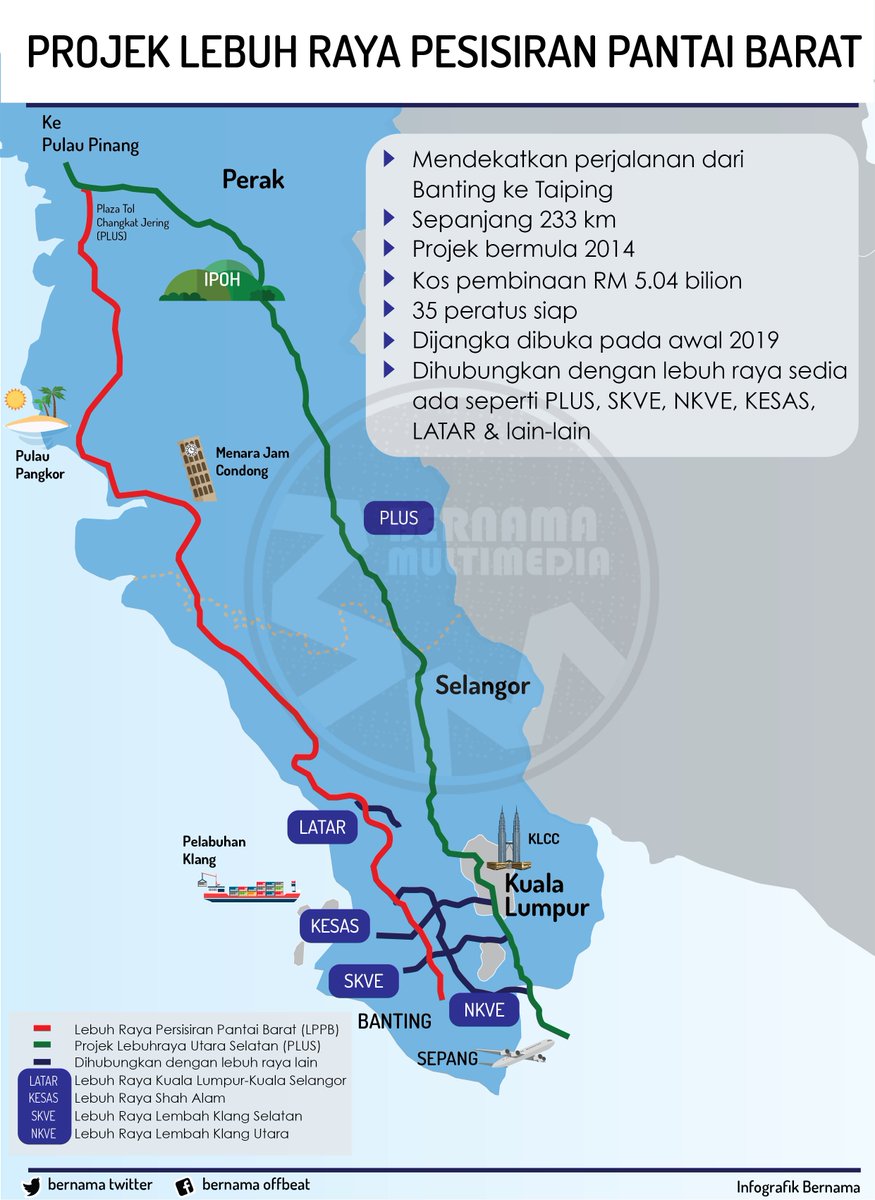

WCEHB is the 80% owner of West Coast Expressway Sdn Bhd, which is contracted to build and operate the 233km highway from Banting in Selangor to Taiping in Perak. Construction is expected to complete in early 2019. 20% is held by IJM.

Here are some maps of the highway.

As we can clearly see, it is likely to be a money maker. It has close links to existing highways and is also likely to eat quite a bit of traffic from PLUS for that particular section, as it’s shorter and have better access to ports.

The Toll Contract

- Concession period is 50 years, with a 10 year extension if the agreed internal rate of return is (IRR) is received.

- IRR agreed is not specified, but the figure is like to be around 10%, Give or take 1%. The IRR for Plus highway is about 10.5% by the way. The absolute bottom is probably something like 8% return.

- Project is likely to cost RM6 billion with an additional RM930 million borne by the government for land acquisition cost.

- Toll revenue in excess of an agreed traffic volume (Additional IRR above agreed rate) will be shared on the basis of 70:30 between the government and WCESB till full settlement of the GSL and subsequently 30:70 after the settlement of the GSL.

The DCF Valuation.

And here, is where everything gets very interesting. From what I’ve noticed, felicity never showed a completed DCF, and let me show you one that I’ve built, using very conservative assumptions.

Assumptions:

- Concession period: 50 years, no extensions.

- IRR: 8%, 9%, 10% and 11%. Assume no sharing with gov as target IRR not hit.

- Traffic Growth rate: Zero (Valautions get very very high once you at in 2% growth rate per annum for 50 years).

- Discount rate: 4.5% (Risk Free Rate in Malaysia)

- Cost of investment: Enterprise value with cash not being deducted, as they are likely to be used for the construction. An additional RM300 million is added, as fund raising may be required due to cost over-runs (calculated by felicity).

- Cost of project: Rm6 billion.

- IJM’s share: 20%

- PBT Margin: 60% as per Litrak and Ekovest

Depending on the IRR chosen. Fair Value is as follows.

IRR 8%: RM2.35

IRR 9%: RM2.62

IRR 10%: RM2.90

IRR 11%: RM3.18

As we can see, at the current price, there is a margin of safety of at least 61% for the worst case scenario. And this valuation assumes zero growth rate. For the record, PLUS growth rate is roughly 2.35% per annum in recent years. If you were to add this in, the valuation becomes obscene even with the profit sharing. But lets stay conservative.

For WCE to be able to generate the PBT indicated by the estimated IRR’s, assuming 60% margin, they will need to generate revenue of RM817 million to RM1.1 billlion. Margins may be a touch higher as the highway is new and lower maintenance is needed, but again, lets be conservative.

Is that revenue achievable? The revenue for PLUS in 2014 is RM3.3 billion. Using the growth rate of 2.35%. Revenue in 2019 is likely to be around RM3.7 billion. WCEHB’s highway will need to take away 22% to 30% of Plus’s revenue. Definitely not unlikely. In addition, some traffic additional traffic is likely to be generated as well, since it the highway flows through the old roads, which consist of people who do not want to take PLUS.

Failure Points

As always, lets invert and find out the failure points for the company and our investment. As Munger always says, find out whats going to kill you and don’t go there.

- Cancellation of the tolls.

This is not really a problem as the government always pays the penalties as stated in the agreement. This can be seen in all current utilities or concession buy backs. As well as the compensation of RM2.2billion paid to PLUS for the cancellation of Kayu Hitam and Batu Tiga tolls.

- Malaysia dying as a country, as it goes down the path of Venezuela if BN wins again.

Well, to be honest, I think that PH will win this round. If they dont, Najib will be dictator life.

But even if BN wins, there is too many capitalistic Chinese in and around this country for that to happen. China is also there to keep Malaysia in check and protect their investment, so it should be ok. Malaysia has a really good geographical potential to be the e-commerce hub for SEA. Either way if BN wins, ill likely pull out some of my investments and move it to Singapore.

- WCEHB bosses cannot be trusted.

IJM is the biggest shareholder of WCEHB. Should not be a problem.

- Can it be completed in time? (ie early 2019)

This one, i’m actually not too sure. Because if it took them 3-4 years to complete 47%, im not sure if they can complete 53% or so 1 year from now. Unless then 47% consist of the hard to build portions, and the 53% is the easy to build ones. We’ll see.

- Can the revenue targets be hit?

This is actually really really hard to know. Unless you have the traffic report, there is no way of knowing with a high level of certainty.

On this one, i have to do what i really dislike.

Rely on the fact the Pang’s and IJM are not retarded. Mamee after being privatized is being fantastically run with a new lease on life. The brand is massively improved, needless to say revenue and profit have also increased massively since the privatization.

I don’t think people like them will put so much money in for 5% IRR or less.

Conclusion

Personally, I quite like this company as a business, and the large margin of safety is also a big plus. Its currently 3% of my portfolio, but I’m definitely seriously considering making it a 10%.

Let me know if you feel i missed out on anything.

Update

In 2018 and 2019, i did some relatively deep research into the Highway Industry in general.

And given the knowledge i know now, i don’t think WCE can hit its revenue or profitability targets.

2 thoughts on “A brief analysis and valuation of WCE Holdings Berhad (WCEHB).”